Frank Breitenbach would like to pull apart the global financial system, while he’s still in it.

And then put it back together again, only this time without credit bubbles, crises and bailouts.

It’s

an old idea that’s receiving fresh impetus in Europe as populism makes

political gains and concern grows about the stability of financial

institutions: Remove from banks the power to create money, and give it

back to the state. Exclusively.

The

proposal has appeal even among some insiders, like Breitenbach. He

couples his day job as a vice president at KfW IPEX in Frankfurt, a

state-owned provider of export financing, with his role as a member of

Monetative, an initiative to return the system to what’s known in German

as Vollgeld, which roughly translates as "whole money."

“There is

too much liquidity in the market now and it’s more or less the same

situation we had right before the 2008 crisis,” Breitenbach said in an

interview on Aug. 12, noting that he was giving his personal views, not

those of KfW. “I have the feeling that another financial crisis will

happen.”

Vollgeld’s solution would be to hand central banks

complete control of the money supply. Commercial banks would be required

to back their loans 100 percent with deposits -- whether they come from

savings, capital or their own borrowings.

In other words, lenders

would be barred from creating money out of nothing -- an inherent

attribute of the fractional-reserve banking model that’s been dominant

since the Middle Ages.

Advocates

of Vollgeld say the change is necessary to prevent the credit booms

that helped cause the last financial bust, and possibly the next.

Central banks would be able to ensure the real economy has the liquidity

it needs, and no more.

“The

amount of money that the central bank will pump into the system should

be in line with economic growth,” Breitenbach said. “It’s the central

bank’s task to take control over the amount of money” in the system, he

said.

While Vollgeld has only a handful of supporters in Germany

-- Breitenbach says his organization has about 100 members -- elsewhere

it’s gathering more steam. A Swiss version has succeeded in gathering

the 100,000 signatures needed to hold a plebiscite on the subject, and a

vote is expected around 2018.

Chicago Plan

That would be

85 years after the first version of Vollgeld was floated, as part of the

Chicago Plan of banking reforms by leading U.S. economists including

Irving Fisher in the wake of the Great Depression. Those ideas were

never implemented, but the continued drag on growth and prosperity from

the 2008 financial crisis is feeding new interest.

Vollgeld’s

counterpart in the U.K. is Positive Money, a group that also advocates

central-bank financing of government expenditure known as “People’s QE.”

A version of that has been backed by Jeremy Corbyn, the leader of the

opposition Labour party.

Adair Turner, former chairman of the

U.K.’s Financial Services Authority, and former Deutsche Bank Chief

Economist Thomas Mayer, have discussed similar ideas.

That’s

not to say Vollgeld will arrive any time soon. For a start, Breitenbach

acknowledges that either it would have to be introduced in the entire

19-nation euro area or a decision taken to break up the single-currency

bloc. Aside from the stability concerns over implementing a new system,

there’s no guarantee that the region’s citizens would trust unelected

monetary officials any more than their commercial counterparts. That’s

especially true in Germany, where the European Central Bank is viewed

with particular skepticism.

Confidence Question

There are other snags. Responding

to the Swiss initiative, the government said Vollgeld wouldn’t prevent

liquidity or solvency problems emerging at lenders. It also pointed out

that allowing the central bank to issue money without a corresponding

rise in assets might undermine public confidence in the central bank, or

in money itself.

For Breitenbach, keeping depositors’ money safe

and stemming a source of bank runs will nevertheless be a huge advance

in stability. And it doesn’t mean destroying the financial system as we

know it.

“I don’t see the contradiction between the Vollgeld

system and being a banker,” he said. “The only difference is that the

banks have to collect savings before lending. ”

That’s a critical

difference, and one Breitenbach argues the general public will find

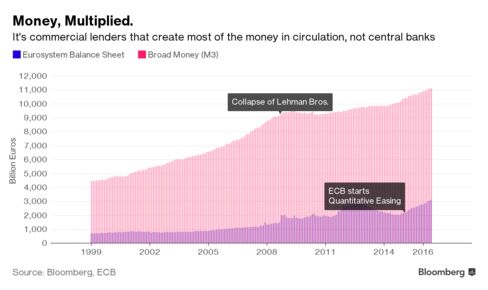

surprising. He says few are aware that it’s actually the commercial

banks that have the largest role in money creation, not the central

bank. Reverse that, and greater stability ensues, goes the thinking.

“The

Vollgeld system is actually much easier to manage than the system we

have right now,” Breitenbach said. “Most people think we already have

this system.”

Nessun commento:

Posta un commento