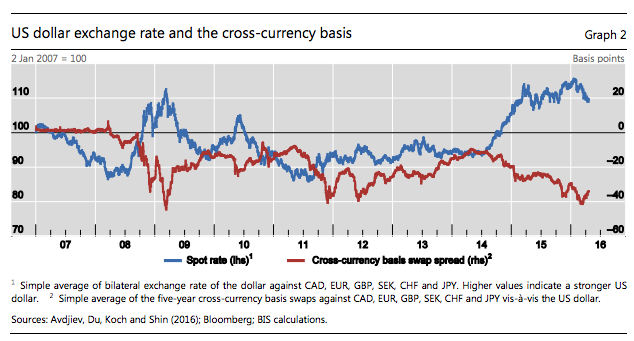

Take a long hard look at this chart:

It comes by way of Hyun Song Shin’s latest piece for the BIS, delivered to a World Bank conference on Wednesday.

Shin describes it as “quite striking”. Though we’re inclined to suggest it’s one of the most important charts in the world right now. And that’s not widely appreciated.

What it shows is how dollar strength and the availability of dollars via the FX swap market go hand-in-hand in the market atm. What it implies is that the global “dollar shortage” is matching if not surpassing 2008 levels.

This follows on from another unprecedented situation occurring in markets: the breakdown of hallowed covered interest parity (CIP) theory, a presumption that interest rates derived from FX swap markets should always be aligned with market rates.

With an FX swap the rate is derived from the cost of pledging your national currency as collateral for access to another type of currency. This, theoretically, should match the rate offered by the market, a.k.a the Libor rate, on the basis that if the rate gets too high, an arbitrage is opened up encouraging those with access to dollars through the Libor market to borrow and then lend out to the FX swap market.

As Shin explains covered interest parity held with barely a blip until the crisis but since then large deviations have been taking place quite regularly. At first these were tied with financial crises. What is remarkable now, says Shin, is that CIP deviations are occurring during periods of relative calm.

Shin hints this may be down to the reduced risk-taking capacity of dealer banks. From Shin:

The reason for this may be down to how the dollar has for decades been recycled through the global banking system. Which is to say, it’s all about the eurodollars (yet again).

Key points to note there: the US dollar is used widely throughout the global banking system, even when neither the lender nor the borrower is a US resident. The dollar is used as an international bridging currency for cross-border transactions, especially in invoicing and trade. It’s used for hedging. It’s also the preferred currency denomination for financing real assets.

What this means is that the universe of dollar-denominated assets extends far beyond the United States, and for large institutional investors with a global portfolio of assets, there may be a currency mismatch between the assets they hold and the commitments they have to their domestic stakeholders.

With payout obligations often in local currencies and assets denominated in dollars, many institutions hedge currency exposures with banks. This sees banks laying off the risk by borrowing dollars in a way that counterbalances the dollar assets with dollar debts.

According to Shin, these factors lead to the following relationship: when the dollar depreciates, banks lend more in US dollars to borrowers outside the US. When the dollar appreciates, however, banks lend less or even shrink outright their lending of dollars.

This gives us a clue about what’s driving the connection between the CIP breakdowns and dollar strength. As Shin observes:

For the US-Europe arm the sums involved have grown from $462bn in 2002 to $1.54tn by 2007 for the US to Europe leg, and from $856bn in 2002 to over $2tn in 2007 for the Europe to US leg.

Notable here is Shin’s point that the round-tripping of dollars between Europe and the United states was one of the ways a large chunk of US subprime mortgages managed to get financed so easily — a fact missed by many economists due to long-standing accounting conventions in international finance, which assume each GDP area has its own currency and that the use of that currency is confined to the same area.

Regarding the mechanics of the round-tripping in question, Shin says:

Once we understand this, we can understand why the dollar’s strengthening since 2014 has had such a profound effect on macroeconomic conditions in emerging markets. It is in essence the equivalent of dollar squeeze for corporates which have leveraged themselves with dollar liabilities in these areas.

What makes matters worse this time, says Shin, is that because the borrowings been done by non financial firms, any associated US dollar-denominated borrowing unwind has the potential to spill over into the real economy much more quickly. This applies even to countries with large FX reserves, because the corporate sector itself may not have access to these dollars.

Add to that the reduced risk taking appetite of banks with access to dollar funds and you’ve got a significant global funding problem on your hands.

Unless, of course, some other hard currency central bank comes to the EM sector’s rescue by lending its currency at rates which more than compensate for swapping the debt out of dollars and into their own currency. Rates which would no doubt have to be negative.

It’s worth noting on that front that Shin says after a slow start the euro is finally beginning to show signs of joining the dollar as an international funding currency.

If you find this turn of events as fascinating as we do, be sure to come to Camp Alphaville on July 1 where Matt Klein will be interviewing Hyun Song Shin about all of the above, and I will be leading a discussion about the critical role of the eurodollar market with Jeffrey Snider, Chief Investment Strategist, Alhambra Investment Partners, Paul Mylchreest, Market Analyst, ADM Investor Services International and Daniela Gabor, Associate Professor, University of the West of England.

Related links:

The petrodollar drawdown quantified – FT Alphaville

The eurodollar as an economic no-man’s land - FT Alphaville

Bearer securities and eurosystems – FT Alphaville

So you thought bearer securities weren’t a thing anymore? – FT Alphaville

All about the eurodollars - FT Alphaville

Eurodollars, China, TIC data + mysteries – FT Alphaville

Petrodollars are eurodollars, and eurodollar base money is shrinking – FT Alphaville

A global reserve requirement for all those eurodollars - FT Alphaville

On the Swiss franc’s non strength – FT Alphaville

On the availability of dollar funding – FT Alphaville

It comes by way of Hyun Song Shin’s latest piece for the BIS, delivered to a World Bank conference on Wednesday.

Shin describes it as “quite striking”. Though we’re inclined to suggest it’s one of the most important charts in the world right now. And that’s not widely appreciated.

What it shows is how dollar strength and the availability of dollars via the FX swap market go hand-in-hand in the market atm. What it implies is that the global “dollar shortage” is matching if not surpassing 2008 levels.

This follows on from another unprecedented situation occurring in markets: the breakdown of hallowed covered interest parity (CIP) theory, a presumption that interest rates derived from FX swap markets should always be aligned with market rates.

With an FX swap the rate is derived from the cost of pledging your national currency as collateral for access to another type of currency. This, theoretically, should match the rate offered by the market, a.k.a the Libor rate, on the basis that if the rate gets too high, an arbitrage is opened up encouraging those with access to dollars through the Libor market to borrow and then lend out to the FX swap market.

As Shin explains covered interest parity held with barely a blip until the crisis but since then large deviations have been taking place quite regularly. At first these were tied with financial crises. What is remarkable now, says Shin, is that CIP deviations are occurring during periods of relative calm.

Shin hints this may be down to the reduced risk-taking capacity of dealer banks. From Shin:

In textbook settings where someone could borrow and lend without limit at prevailing market interest rates, the cross-currency basis could not deviate from zero, at least not by much, and not for too long. This is because someone could borrow at the cheaper dollar interest rate and lend out at the higher dollar interest rate. However, executing such a trade entails a sequence of transactions, often through intermediaries. As such, it makes demands on the risk-taking capacity of dealer banks as well as counterparties.From Shin’s perspective, what’s really glaring however is that dollar strength is impacting not just emerging markets but other hard currencies zones as well, especially “safe haven” currencies such as the yen and the Swiss franc.

The reason for this may be down to how the dollar has for decades been recycled through the global banking system. Which is to say, it’s all about the eurodollars (yet again).

Key points to note there: the US dollar is used widely throughout the global banking system, even when neither the lender nor the borrower is a US resident. The dollar is used as an international bridging currency for cross-border transactions, especially in invoicing and trade. It’s used for hedging. It’s also the preferred currency denomination for financing real assets.

What this means is that the universe of dollar-denominated assets extends far beyond the United States, and for large institutional investors with a global portfolio of assets, there may be a currency mismatch between the assets they hold and the commitments they have to their domestic stakeholders.

With payout obligations often in local currencies and assets denominated in dollars, many institutions hedge currency exposures with banks. This sees banks laying off the risk by borrowing dollars in a way that counterbalances the dollar assets with dollar debts.

According to Shin, these factors lead to the following relationship: when the dollar depreciates, banks lend more in US dollars to borrowers outside the US. When the dollar appreciates, however, banks lend less or even shrink outright their lending of dollars.

This gives us a clue about what’s driving the connection between the CIP breakdowns and dollar strength. As Shin observes:

The breakdown of covered interest parity is a symptom of tighter dollar credit conditions putting a squeeze on accumulated dollar liabilities built up during the previous period of easy dollar credit. During the period of dollar weakness, global banks were able to supply hedging services to institutional investors at reasonable cost, as cross-border dollar credit was growing strongly and easily obtained. However, as the dollar strengthens, the banking sector finds it more challenging to roll over the dollar credit previously supplied.All of which has helped to intensify dollar recycling flows around the world, and in particular the two-way flow between Europe and the US, which has always been the most prominent:

For the US-Europe arm the sums involved have grown from $462bn in 2002 to $1.54tn by 2007 for the US to Europe leg, and from $856bn in 2002 to over $2tn in 2007 for the Europe to US leg.

Notable here is Shin’s point that the round-tripping of dollars between Europe and the United states was one of the ways a large chunk of US subprime mortgages managed to get financed so easily — a fact missed by many economists due to long-standing accounting conventions in international finance, which assume each GDP area has its own currency and that the use of that currency is confined to the same area.

Regarding the mechanics of the round-tripping in question, Shin says:

The two-way flow resulted from the “round-tripping” of dollars intermediated by the large European banks which raised wholesale funds by using their US branches to borrow from US money market funds, ship the funds back to headquarters and then recycle the proceeds back to the United States by purchasing securities built on mortgages of US households.But while the strengthening of the dollar since mid-2014 brings us back full circle to mechanisms at play in the round-tripping scenario, the paradigm may have shifted. The key protagonists are no longer European banks but emerging market corporates and the borrowing is done through corporate bonds rather than wholesale bank funding.

Once we understand this, we can understand why the dollar’s strengthening since 2014 has had such a profound effect on macroeconomic conditions in emerging markets. It is in essence the equivalent of dollar squeeze for corporates which have leveraged themselves with dollar liabilities in these areas.

What makes matters worse this time, says Shin, is that because the borrowings been done by non financial firms, any associated US dollar-denominated borrowing unwind has the potential to spill over into the real economy much more quickly. This applies even to countries with large FX reserves, because the corporate sector itself may not have access to these dollars.

Add to that the reduced risk taking appetite of banks with access to dollar funds and you’ve got a significant global funding problem on your hands.

Unless, of course, some other hard currency central bank comes to the EM sector’s rescue by lending its currency at rates which more than compensate for swapping the debt out of dollars and into their own currency. Rates which would no doubt have to be negative.

It’s worth noting on that front that Shin says after a slow start the euro is finally beginning to show signs of joining the dollar as an international funding currency.

To be sure, the sums are still small for the euro. The stock of euro-denominated debt of non-banks outside the euro area is only around a quarter of the equivalent US dollar amount. But the trajectory is steep. US companies have been particularly active in borrowing in euros.Which, of course, is what the architects of the euro currency always wanted (dare we say).

If you find this turn of events as fascinating as we do, be sure to come to Camp Alphaville on July 1 where Matt Klein will be interviewing Hyun Song Shin about all of the above, and I will be leading a discussion about the critical role of the eurodollar market with Jeffrey Snider, Chief Investment Strategist, Alhambra Investment Partners, Paul Mylchreest, Market Analyst, ADM Investor Services International and Daniela Gabor, Associate Professor, University of the West of England.

Related links:

The petrodollar drawdown quantified – FT Alphaville

The eurodollar as an economic no-man’s land - FT Alphaville

Bearer securities and eurosystems – FT Alphaville

So you thought bearer securities weren’t a thing anymore? – FT Alphaville

All about the eurodollars - FT Alphaville

Eurodollars, China, TIC data + mysteries – FT Alphaville

Petrodollars are eurodollars, and eurodollar base money is shrinking – FT Alphaville

A global reserve requirement for all those eurodollars - FT Alphaville

On the Swiss franc’s non strength – FT Alphaville

On the availability of dollar funding – FT Alphaville

Nessun commento:

Posta un commento