The President of the European Central Bank Mario Draghi is on his way out. Photographer: Stringer/AFP/Getty Images

To get John Authers' newsletter delivered directly to your inbox, sign up here.

Max Headroom to do whatever it takes.

When European Central Bank President Mario Draghi speaks, markets

usually take notice. Back in 2012, he effectively ended the euro zone’s

sovereign debt crisis by promising to do “whatever it takes” to protect

the euro. His words were so effective that the market never tested his

resolve. The crisis abated, even as the economy went into a long and

slow malaise.

On the face of it, his comments after the ECB monetary policy

meeting Thursday, held this month in Lithuania, were almost as

aggressive as those he spoke in 2012. He was obviously determined to

convince all that he was prepared to be far more dovish if necessary. He

even suggested that he had “headroom” to resort to more quantitative

easing, or bond purchases, if necessary. And yet the market did not take him all that seriously.

The euro somehow strengthened against the dollar, exactly the opposite

of what should happen when a central banker hints at interest rate cuts.

This is partly because Draghi is half way out the door,

as Bloomberg Opinion columnist Ferdinando Giugliano put it. It is also

because the ECB is running out of ammunition. Rates are already low, and

its balance sheet is loaded. It does not have anything like as much

freedom of movement as the Federal Reserve. The need to do something is

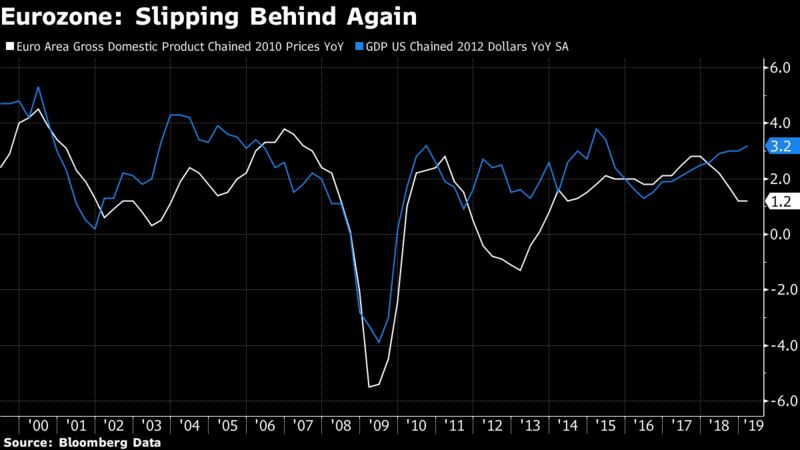

clear enough. The euro zone’s economy has not lagged behind the U.S. as

badly as many believe since the single currency came into being in 1999,

but the latest dip, while the U.S. is gaining strength, is concerning.

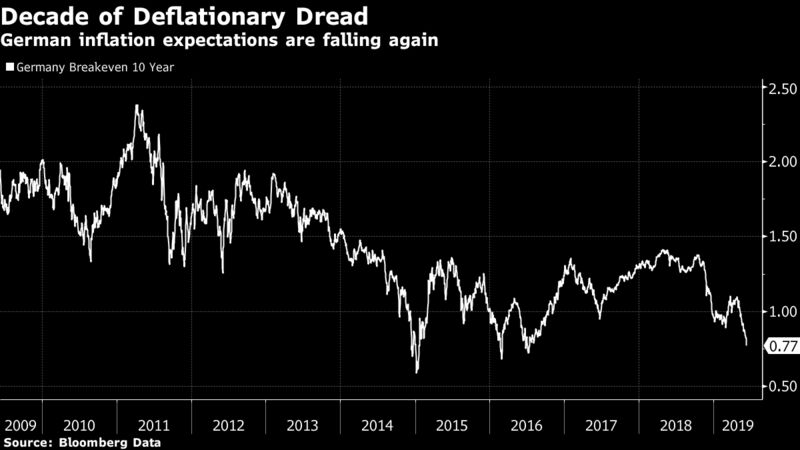

Another

problem is that inflationary expectations appear to have become

untethered. The German bund market is signaling inflation of less than

0.8% per year over the next 10 years. This is lower than at any point

when the sovereign debt crisis was at its height, from 2010 to 2012, and

approaching its lowest since the euro’s inception. The ECB has another

deflation scare on its hands:

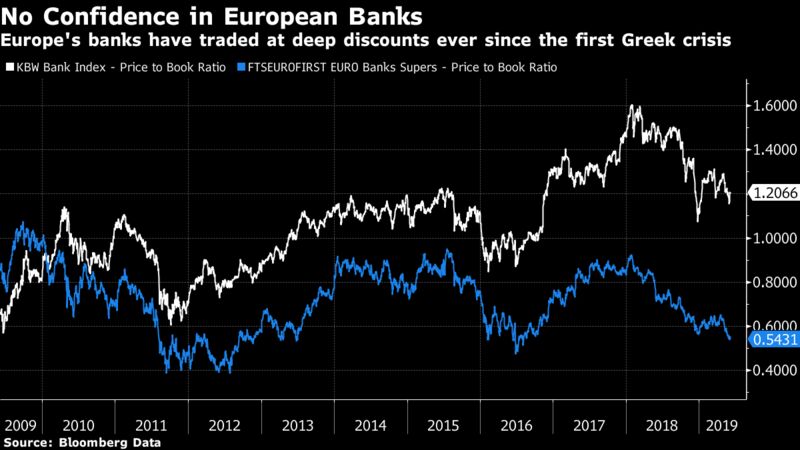

The

Achilles heel responsible for Europe’s relative weakness is its banking

system. The price-to-book multiple that shareholders pay for

bank shares is as good an indicator of this as any. Ever since the first

Greece bailout crisis broke out in early 2010, European banks have

traded at a discount to their book value, and a big discount to banks in

the U.S. This explains why the ECB needs to keep propping up the

banking system with targeted help. But as it wants to avoid moral

hazard, that help cannot be too generous, which is why I found the plans

for the latest “TLTRO” loan program to shore up banks rather

unconvincing.

There

is a decent argument that pessimism towards the euro zone has become

excessive. But with the real possibility that we will have to wait

months to learn the identity of Draghi’s successor – he is due to leave

at the end of October, just when the U.K. is due to leave the EU – there

is a nasty tail risk from the euro zone to look forward to over the

summer.

Nessun commento:

Posta un commento