QE: quantitatively shrinking collateral reuse

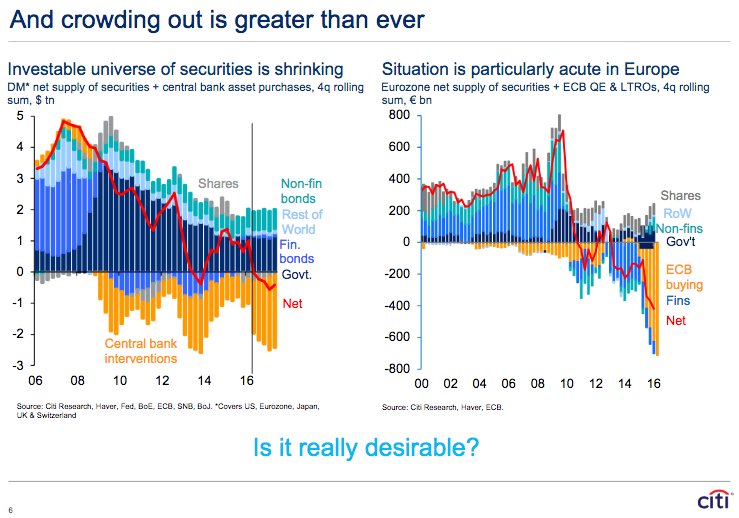

Adding to the QE scarcity concerns already highlighted by David earlier on Monday, here’s a couple of charts from Citi’s Hans Lorenzen reflecting the fundamental “too much of a good thing” problem with QE.

Glaring, right?

As has been frequently mentioned to us by the IMF’s resident collateral expert Manmohan Singh, when the central bank becomes the market for quality collateral in the context of regulatory policy which restricts collateral re-use for macro-prudential reasons, this technically amounts to the very same thing as narrow money policy.

In Singh’s opinion, the only thing which can consequently return the collateral and repo markets to a normal state of functionality is a strategic decision to allow collateral held on central bank balance sheets to be actively reused in the market.

As Singh has explained to us, in economic terms the “reuse” or rehypothecation of a security is identical to the money creation that takes place in commercial banking through the process of accepting deposits and making loans. That’s why restricting collateral reuse even in the context of ample QE still has the end result of tightening monetary policy all round (especially in a world where bank reserves, which are only accessible to licensed banks, might be deemed an inferior final settlement security than T-bills).

The key differentiator between high quality collateral and bank reserves, which leads to its superior and final settlement characteristic, is of course its cross-border nature.

As Singh notes, if we understand that the term “pledged for reuse” constitutes the equivalent of collateral which can be reused by the taker in his own name, we can see how and why the practice comes to underpin the economies of scale provided to the market by the financial system. We’d even argue this is precisely what banking is supposed to be about: the efficient and productive reuse of other people’s idle capital for the purpose of extending the longevity and duration of underlying savings.

At the same time, however, it’s undeniable the practice creates multiple current claims over the same securities, posing macro-prudential risks which lead to intermittent financial panics if and when the reuse merry-go-round ever comes to an abrupt halt. And so it is, understandably, that regulators and central bankers come to see the reuse of collateral as the source of risk in the financial system and strive to limit its intensity.

The problem is, if finance really is all about the risky re-use of scarce capital for the sake of economic scaling, then shuttering the industry’s capacity to reuse collateral defies its raison d’etre and inevitably impacts its return potential.

Once we understand this, it’s easy to comprehend how and why central banks got into the stealth act of re-lending gold collateral to the point that conspiracy theories about them not physically owning any of the gold they claimed to own became common place. It wasn’t the product of a sinister conspiracy. It was the simple need to put that gold to work in a way that allowed the financial sector to re-establish its raison d’etre.

In a globalised financial system, forcing banks to restrict collateral reuse to the domain of bank reserves — which are national and central bank controlled — in lieu of internationally accepted collateral which can be endogenously re-lent according to market demand inevitably deprives the global financial system of liquidity. Not only that, it creates an incentive for the market to turn to new and arguably riskier “safe assets” for the purpose of cross-border rehypothecation.

Whether that’s a bad thing, we don’t know. Perhaps the international financial system should be underpinned by privately originated safe assets as opposed to those created by the public balance sheets of hard-currency issuing states, which are then put in the uncomfortable position of having to honour over-extended claims they themselves didn’t create? But then the question remains, can the international financial system achieve the same reuse intensity if and when the underlying collateral it’s using for final settlement isn’t backed by a public purse?

Update: As Daniela Gabor notes on Twitter, it should be pointed out that some central banks (ECB ahem) have started lending out collateral precisely to address these constraints. But the argument outlined above relates to the fact that the reuse rate is still insufficient to make a real difference and that the reuse terms (max 30 days and maximum 200m per counterparty according to Gus Baratta) aren’t permanent enough to induce the scale of lubrication needed by the market.

Related links

ECB warnings and yield target allusions - FT Alphaville

Are reserves still “special”? – Bank Underground

The eurodollar as an economic no-man’s land – FT Alphaville

How do you solve a problem like de-globalisation? – FT Alphaville

As goes correspondent banking, so goes globalisation – FT Alphaville

Glaring, right?

As has been frequently mentioned to us by the IMF’s resident collateral expert Manmohan Singh, when the central bank becomes the market for quality collateral in the context of regulatory policy which restricts collateral re-use for macro-prudential reasons, this technically amounts to the very same thing as narrow money policy.

In Singh’s opinion, the only thing which can consequently return the collateral and repo markets to a normal state of functionality is a strategic decision to allow collateral held on central bank balance sheets to be actively reused in the market.

As Singh has explained to us, in economic terms the “reuse” or rehypothecation of a security is identical to the money creation that takes place in commercial banking through the process of accepting deposits and making loans. That’s why restricting collateral reuse even in the context of ample QE still has the end result of tightening monetary policy all round (especially in a world where bank reserves, which are only accessible to licensed banks, might be deemed an inferior final settlement security than T-bills).

The key differentiator between high quality collateral and bank reserves, which leads to its superior and final settlement characteristic, is of course its cross-border nature.

As Singh notes, if we understand that the term “pledged for reuse” constitutes the equivalent of collateral which can be reused by the taker in his own name, we can see how and why the practice comes to underpin the economies of scale provided to the market by the financial system. We’d even argue this is precisely what banking is supposed to be about: the efficient and productive reuse of other people’s idle capital for the purpose of extending the longevity and duration of underlying savings.

At the same time, however, it’s undeniable the practice creates multiple current claims over the same securities, posing macro-prudential risks which lead to intermittent financial panics if and when the reuse merry-go-round ever comes to an abrupt halt. And so it is, understandably, that regulators and central bankers come to see the reuse of collateral as the source of risk in the financial system and strive to limit its intensity.

The problem is, if finance really is all about the risky re-use of scarce capital for the sake of economic scaling, then shuttering the industry’s capacity to reuse collateral defies its raison d’etre and inevitably impacts its return potential.

Once we understand this, it’s easy to comprehend how and why central banks got into the stealth act of re-lending gold collateral to the point that conspiracy theories about them not physically owning any of the gold they claimed to own became common place. It wasn’t the product of a sinister conspiracy. It was the simple need to put that gold to work in a way that allowed the financial sector to re-establish its raison d’etre.

In a globalised financial system, forcing banks to restrict collateral reuse to the domain of bank reserves — which are national and central bank controlled — in lieu of internationally accepted collateral which can be endogenously re-lent according to market demand inevitably deprives the global financial system of liquidity. Not only that, it creates an incentive for the market to turn to new and arguably riskier “safe assets” for the purpose of cross-border rehypothecation.

Whether that’s a bad thing, we don’t know. Perhaps the international financial system should be underpinned by privately originated safe assets as opposed to those created by the public balance sheets of hard-currency issuing states, which are then put in the uncomfortable position of having to honour over-extended claims they themselves didn’t create? But then the question remains, can the international financial system achieve the same reuse intensity if and when the underlying collateral it’s using for final settlement isn’t backed by a public purse?

Update: As Daniela Gabor notes on Twitter, it should be pointed out that some central banks (ECB ahem) have started lending out collateral precisely to address these constraints. But the argument outlined above relates to the fact that the reuse rate is still insufficient to make a real difference and that the reuse terms (max 30 days and maximum 200m per counterparty according to Gus Baratta) aren’t permanent enough to induce the scale of lubrication needed by the market.

Related links

ECB warnings and yield target allusions - FT Alphaville

Are reserves still “special”? – Bank Underground

The eurodollar as an economic no-man’s land – FT Alphaville

How do you solve a problem like de-globalisation? – FT Alphaville

As goes correspondent banking, so goes globalisation – FT Alphaville

Nessun commento:

Posta un commento