Something doesn’t add up in the world.

And when things don’t add up, you can only really blame the accountants.

Here’s the problem.

As per Gabriel Zucman’s book, The Hidden Wealth of Nations, the world’s financial liabilities are worth about $7.6 trillion more than the world’s financial assets. Roughly $6.1 trillion of these extra liabilities take the form of equity and long-term debt, with the other $1.5 trillion held in low-yielding deposits and money-market funds.

As FT Alphaville’s Matt Klein has pointed out already there are only three possible explanations for such a massive discrepancy:

Zucman tells us nobody really knows for sure because before 2001 many countries didn’t report complete portfolio asset positions which messes with the statistics.

Nevertheless, our first hint of something being mismatched comes about in the 1970s when the IMF first began noticing the world was running a current account deficit, says Zucman.

As the IMF noted in a report in 2000:

But the 1970s start-point is interesting for other reasons.

Mariana Mazucatto, innovation economist at Sussex University, reminded us last week that GDP statistics only began to include financial rent as an added-value contribution to global productivity in the 1960s.

We started wondering whether this could have had some bearing on the discrepancy between global liabilities and assets.

As the IMF noted in 2000:

On one hand we have the underreporting of investment income potentially contributing to a global asset/liability discrepancy, implying some portion of global wealth is being hidden for tax purposes or because it’s derived from illegal sources (a meth lab is a risky asset, but still an asset, as is a gun in the hand of an extortionist).

On the other hand, we formalised the manner in which investment and financial rent might be inputted into the system as a value-add. The latter would imply a boost to the asset side of the equation not a contraction, one would think?

In 1997, the IMF observed that it was the 1987 current account study’s focus on investment income transactions, which include interest and dividend earnings and payments, which had drawn attention to the discrepancy:

Money as the product of a financial firm

As noted earlier, financial rent began to be featured as a value-add component in GDP in the 1960s, according to Mazzucato. Even so, the methodology behind this inclusion — which focuses on the net interest margin — has always been strongly challenged. Some have argued, for example, that because the interest margin includes a risk premium, a large amount of what’s being counted as value add might very well be being over-estimated. The counter argument, of course, is that the core value-add service banks provide is screening for investor risk and hunting out information advantages.

As the BoE’s quarterly bulletin in 2011 noted:

Diana Hancock, of the Federal Reserve, observed in her seminal piece on banks as financial firms, in 1985, that banks were in fact producers of monetary goods. Like conventional producers they too had an interest in withholding supply if and when returns fell below productions costs. The only difference is that banks as a rule have much lower production costs than traditional firms, amounting mostly to the cost of screening and verifying investments; their own as well as other players who they see fit to bring into their “eco-systems” for the sake of transaction fungibility.

In the topsy turvy world of monetary goods, consequently, the cost of production is directly linked to the cost of screening risk in the system and pricing it in accordance to the overall quantity of capital available in the economy.

If that’s true, marketshare, can only be gained if bankers are prepared to be less thorough with screening or take a contrarian view on how much capital there really is to go around. For the most part that makes “disruptor” money producers riskier entities as a whole, solidifying the cartel structure of the initial stakeholding network.

As Hancock notes:

Money is a risk-sharing technology. When it works it transfers risk to those most willing and able to bear it and helps households and investors insure against the unexpected. When it doesn’t (very much like modern information technology platforms) it transfers risk — in some cases educated risk — to those least willing and able to bear it by forcing households and investors to cover losses when the value which was perceived as having been added is suddenly removed by constantly adjusting market dynamics.

Like Uber, banking works by getting others to absorb the risk of variable returns whilst taking a steady fee for itself for as long as it able to.

For as long as positive and negative value are conflated via the bank intermediation process, however, there’s an argument to be made that today’s financial accounting isn’t fit for purpose. We simply have no idea whether the assets being created by the banking sector are not being simultaneously offset by additional risks in the system elsewhere.

Going back to Zucman, should we really be surprised that there are outstanding liabilities versus creditor assets, if financial intermediaries are predisposed to overcharging for risk services before they have actually been proven to add value?

Once everything is squared up, after all, that’s tantamount to a significant number of non-asset-backed liabilities in the system, funded as it were by yet-to-be created future value rather than existing capital — a factor exaggerated by rising interest rates and the capacity of offshore centres to obscure unfunded liability creation.

Related links:

The bond liquidity ‘cognitive bandwidth deficit’ problem – FT Alphaville

And when things don’t add up, you can only really blame the accountants.

Here’s the problem.

As per Gabriel Zucman’s book, The Hidden Wealth of Nations, the world’s financial liabilities are worth about $7.6 trillion more than the world’s financial assets. Roughly $6.1 trillion of these extra liabilities take the form of equity and long-term debt, with the other $1.5 trillion held in low-yielding deposits and money-market funds.

As FT Alphaville’s Matt Klein has pointed out already there are only three possible explanations for such a massive discrepancy:

So, how long has this mismatch been a thing?

- aliens have been accumulating trillions of dollars of claims against Earthlings

- innocent mistakes by statistical agencies add up to an enormous gap, or, most believably

- the world’s ultra-rich have squirrelled away trillions of dollars from the authorities to avoid paying tax.

Zucman tells us nobody really knows for sure because before 2001 many countries didn’t report complete portfolio asset positions which messes with the statistics.

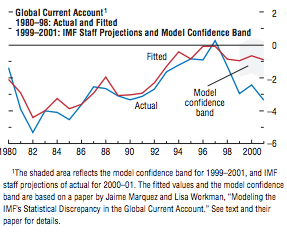

Nevertheless, our first hint of something being mismatched comes about in the 1970s when the IMF first began noticing the world was running a current account deficit, says Zucman.

As the IMF noted in a report in 2000:

In principle, since the exports of one country are the imports of another, the current account balances of all countries in the world should sum to zero. In practice, however, this is not the case. Since the mid-1970s, the sum of all countries’ current account balances has—except in 1997—been negative, giving the world in aggregate a measured current account deficit.As to the largest contributing factor to that global deficit? According to the IMF, that was the investment income account, with smaller, but still significant deficits on the transfers account, caused by four main factors: transportation delays (call that the stuff in “limbo” effect), asymmetric valuation (mis-valuation at import/export point due to fluctuating FX rates), data quality (book-keeping errors) and… underreporting of investment income.

In 1998, the last year for which complete data are available, this global current account discrepancy was about 1 percent of world imports, but preliminary data suggest that it increased sharply to 3 percent of world imports in 1999. Such a large and variable current account discrepancy is of particular concern at a time when substantial external current account imbalances in the three main currency areas are a major policy issue.

But the 1970s start-point is interesting for other reasons.

Mariana Mazucatto, innovation economist at Sussex University, reminded us last week that GDP statistics only began to include financial rent as an added-value contribution to global productivity in the 1960s.

We started wondering whether this could have had some bearing on the discrepancy between global liabilities and assets.

As the IMF noted in 2000:

Investment income is difficult to capture and therefore may go underreported in the balance of payments. The growth of offshore financial centers is making it more difficult for statistical agencies to track financial transactions.A paradox, surely?

On one hand we have the underreporting of investment income potentially contributing to a global asset/liability discrepancy, implying some portion of global wealth is being hidden for tax purposes or because it’s derived from illegal sources (a meth lab is a risky asset, but still an asset, as is a gun in the hand of an extortionist).

On the other hand, we formalised the manner in which investment and financial rent might be inputted into the system as a value-add. The latter would imply a boost to the asset side of the equation not a contraction, one would think?

In 1997, the IMF observed that it was the 1987 current account study’s focus on investment income transactions, which include interest and dividend earnings and payments, which had drawn attention to the discrepancy:

The discrepancy between investment income credits and debits (excluding reinvested earnings from direct investment) has steadily increased since then to become the largest contributor to the overall discrepancy in the world current accounts.The IMF had basically noticed that a large body of cross-border assets were being recognised by debtor countries but not, for some reason, by the creditor countries, a condition which only got worse as interest rates rose after 1979. Countries receiving the capital, the IMF proposed, were perhaps in a better position to measure capital inflows than countries where the creditors resided.

Money as the product of a financial firm

As noted earlier, financial rent began to be featured as a value-add component in GDP in the 1960s, according to Mazzucato. Even so, the methodology behind this inclusion — which focuses on the net interest margin — has always been strongly challenged. Some have argued, for example, that because the interest margin includes a risk premium, a large amount of what’s being counted as value add might very well be being over-estimated. The counter argument, of course, is that the core value-add service banks provide is screening for investor risk and hunting out information advantages.

As the BoE’s quarterly bulletin in 2011 noted:

But it is hard to quantify the benefits arising when banks use this additional information. Banks with better risk management practices should be regarded as providing higher-quality services, and therefore as generating higher output when they provide finance. But this activity is almost impossible to measure ex ante. Conversely, the impact of poor decision-making may only become apparent years later, and cannot easily be reflected in estimates of output when a loan is first made.This thinking adds to the thesis that finance is ultimately a production technology which uses data as an input, processes said data, and transforms it into a decision as to where to allocate capital profitably and without risk.

Diana Hancock, of the Federal Reserve, observed in her seminal piece on banks as financial firms, in 1985, that banks were in fact producers of monetary goods. Like conventional producers they too had an interest in withholding supply if and when returns fell below productions costs. The only difference is that banks as a rule have much lower production costs than traditional firms, amounting mostly to the cost of screening and verifying investments; their own as well as other players who they see fit to bring into their “eco-systems” for the sake of transaction fungibility.

In the topsy turvy world of monetary goods, consequently, the cost of production is directly linked to the cost of screening risk in the system and pricing it in accordance to the overall quantity of capital available in the economy.

If that’s true, marketshare, can only be gained if bankers are prepared to be less thorough with screening or take a contrarian view on how much capital there really is to go around. For the most part that makes “disruptor” money producers riskier entities as a whole, solidifying the cartel structure of the initial stakeholding network.

As Hancock notes:

The financial firm maximises a function based on the utility of variable profits, and the response of monetary production depends on the attitude toward risk and the specification of the utility function.Should negative and positive values be fungible?

Money is a risk-sharing technology. When it works it transfers risk to those most willing and able to bear it and helps households and investors insure against the unexpected. When it doesn’t (very much like modern information technology platforms) it transfers risk — in some cases educated risk — to those least willing and able to bear it by forcing households and investors to cover losses when the value which was perceived as having been added is suddenly removed by constantly adjusting market dynamics.

Like Uber, banking works by getting others to absorb the risk of variable returns whilst taking a steady fee for itself for as long as it able to.

For as long as positive and negative value are conflated via the bank intermediation process, however, there’s an argument to be made that today’s financial accounting isn’t fit for purpose. We simply have no idea whether the assets being created by the banking sector are not being simultaneously offset by additional risks in the system elsewhere.

Going back to Zucman, should we really be surprised that there are outstanding liabilities versus creditor assets, if financial intermediaries are predisposed to overcharging for risk services before they have actually been proven to add value?

Once everything is squared up, after all, that’s tantamount to a significant number of non-asset-backed liabilities in the system, funded as it were by yet-to-be created future value rather than existing capital — a factor exaggerated by rising interest rates and the capacity of offshore centres to obscure unfunded liability creation.

Related links:

The bond liquidity ‘cognitive bandwidth deficit’ problem – FT Alphaville

Nessun commento:

Posta un commento