All about the eurodollars, redux

You may have seen our work on the hypothetical eventuality of no

more petrodollars, eurodollars, sweatdollars and all other forms of

offshore recycled dollars here, here and here.

You may also have seen our coverage of the technical overvaluation of the yuan and the upcoming capital outflow problem here, here and here.

And last of all, you may have seen how we think it all connects together here.

For those who didn’t, Paul Mylchreest at ADM Investor Services International — who it must be flagged has a certain gold-loving disposition– has been nice enough to consolidate a lot of our thinking in a new report on the impact of diminishing eurodollars in the system. A sizeable snippet (our emphasis):

That charts runs only until 2010.

But here’s the big reveal with what’s been happening since then:

Mylchreest says that whilst he could be wrong it looks to him like there’s been a clear run on eurodollar liquidity to rival that of 2007-2008 on at least three occasions, based on the Treasury International Capital (TIC) measure of capital flows. Just to isolate those points precisely, they fell on the following three occasions:

Mylchreest reminds us that the SNB attributed their surprise move to abandon a EUR/CHF floor policy to central bank policy divergence and dollar strength in their statement:

Related links:

Unravelling Russia’s offshore financial nexus (updated) – FT Alphaville

All about the eurodollars, China edition – FT Alphaville

All about the eurodollars – FT Alphaville

The theory of money entanglement (Part 2) – FT Alphaville

The Euro-Dollar Market: Some First Principles – Milton Friedman

BIS says we should follow the money – FT Alphaville

With petrodollars also go global reserves – FT Alphaville

On the hypothetical eventuality of no more petrodollars – FT Alphaville

Hello world. I’m the PetroEuro! – FT Alphaville

You may also have seen our coverage of the technical overvaluation of the yuan and the upcoming capital outflow problem here, here and here.

And last of all, you may have seen how we think it all connects together here.

For those who didn’t, Paul Mylchreest at ADM Investor Services International — who it must be flagged has a certain gold-loving disposition– has been nice enough to consolidate a lot of our thinking in a new report on the impact of diminishing eurodollars in the system. A sizeable snippet (our emphasis):

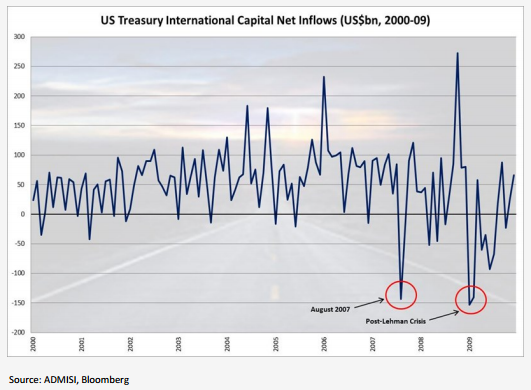

Our analysis suggests that there is an emerging Eurodollar liquidity shortage – which extends into wholesale and shadow banking markets – and is exacerbated by currency/maturity mismatch. Eurodollars are dollar deposits held in offshore accounts outside the US. Regulatory change and Fed policy (QE 2/QE 3) contributed to the tightness in Eurodollar liquidity, leading to a huge inflow of dollars (US$1.0 trillion) on the part of foreign banks from offshore Eurodollar markets into domestic US money markets in 2011-14. The recent reversal suggests that foreign banks might be trying to shore up Eurodollar operations. It is looking increasingly like the Eurodollar is taking on a role akin to a “Global Fed Funds rate.” Investors may have underestimated the degree to which a rising dollar transmits tighter monetary policy across an already misfiring global economy, especially when it is carrying US$10 trillion (+70% since 2008) in offshore Eurodollar debt. From a Chinese (especially) and EM standpoint in particular, it is becoming increasingly clear that the dollar has been “weaponised.”Mylchreest in any case offers up the following chart, which he says shows the eurodollar shortage popping up in the monthly Treasury International Capital data by way of net dollar outflows in August 2007 and end-2008/start-2009:

While the Fed is using existing bilateral agreements to expand much-needed dollar swaps to other DM central banks (likely including the Bank of England on a covert basis…for HSBC or Standard Chartered we wonder?), the lack of a dollar swap arrangement with the PBoC is a glaring omission. We believe that the Chinese sell-off in foreign exchange reserves and US Treasuries has been more to do with providing wholesale Eurodollar liquidity to its banking system, rather than supporting the peg per se. This is harming stability and risks stoking a deterioration in relations between China and the US over the “dollar issue.”

That charts runs only until 2010.

But here’s the big reveal with what’s been happening since then:

Mylchreest says that whilst he could be wrong it looks to him like there’s been a clear run on eurodollar liquidity to rival that of 2007-2008 on at least three occasions, based on the Treasury International Capital (TIC) measure of capital flows. Just to isolate those points precisely, they fell on the following three occasions:

Also worth noting, the overnight Libor rate — the cost of borrowing eurodollars overnight — bottomed out around the beginning of 2014 as well.

- The beginning of 2014 – just prior to initial Yuan devaluation (see below);

- Mid-2014 – when so many economic indicators changed direction and the dollar began its major rise; and

- End-2014 – when foreign banks suddenly moved about US300bn overseas from US money markets.

Mylchreest reminds us that the SNB attributed their surprise move to abandon a EUR/CHF floor policy to central bank policy divergence and dollar strength in their statement:

“Recently, divergences between the monetary policies of the major currency areas have increased significantly – a trend that is likely to become even more pronounced. The euro has depreciated considerably against the US dollar and this, in turn, has caused the Swiss franc to weaken against the US dollar.”To conclude, Mylchreest worries that the the rest of the world may now be running US dollar short worth up to $10tn.

Related links:

Unravelling Russia’s offshore financial nexus (updated) – FT Alphaville

All about the eurodollars, China edition – FT Alphaville

All about the eurodollars – FT Alphaville

The theory of money entanglement (Part 2) – FT Alphaville

The Euro-Dollar Market: Some First Principles – Milton Friedman

BIS says we should follow the money – FT Alphaville

With petrodollars also go global reserves – FT Alphaville

On the hypothetical eventuality of no more petrodollars – FT Alphaville

Hello world. I’m the PetroEuro! – FT Alphaville

Nessun commento:

Posta un commento