domenica 5 giugno 2016

sabato 4 giugno 2016

Stiglitz: Ban offshore banks with account secrecy

Ban offshore banks with account secrecy from US correspondent accounts says Nobel laureate Joseph Stiglitz

Filed under Blog, offshore, tax evasion. You can follow any responses to this entry through the RSS 2.0. You can leave a response or trackback to this entryhttp://www.thekomisarscoop.com/2016/06/ban-offshore-banks-with-account-secrecy-from-us-correspondent-accounts-says-nobel-laureate-joseph-stiglitz/

Joe Stiglitz, why do we have offshore banking.

At the breakfast on “Is U.S. Finance Hurting Growth?”, he addressed an aspect of banking that was not on the agenda, asking, “Why do we have offshore banking? You know, is it that finance really does better in the Cayman Islands because of the sunshine? (Laughter.) You know, that makes money grow faster.”

Lucy asks how would you shut it down?

“So the question is, why don’t we just shut it down?

At question time, I said, “I’ve written for many years about the offshore bank and corporate secrecy system. So I’d like to ask Joe, how would you shut it down?”

He replied, “Well, in a way I’m—this picks up a little bit on … what we did in the Anti-Terror Act, you know. We did really—we cut off correspondence relationships. It had some adverse effects on some countries, but it had—it worked. The system of financing for terrorism really—I think it was an effective system. So if we had a resolve to do it, and there would be a debate about the collateral damage ….it would be worth doing precisely things like the correspondence banking.”

Stiglitz says US should require standards for correspondent relationships.

After the meeting, I asked Prof. Stiglitz, “How would you use the corresponding banking system to shut offshore down?”

He said, “You [say you] can’t have a correspondent relationship with the US if you aren’t a compliant client bank.”

He explained, “The US government would say, ‘Here are standards, if you don’t meet those standards….’ We have standards that now don’t include [this.]”

I pointed out that Treasury has OFAC [Office of Foreign Assets Control] used to ban US financial connections to banks deemed to help terrorists. Prof. Stiglitz said, “That’s the spirit. They haven’t extended it to this broader sense of tax havens.”

He added, “Onshore bad behavior is as bad as offshore, and we haven’t come to grips with that. Now Panama has better, higher standards than Delaware in many of these issues. Treasury could do something about that.”

He noted that, “To give you one example, Treasury is now requiring the disclosure of beneficial ownership of real estate transactions in New York City and Washington. But not elsewhere. Why did they….We know why they chose those places. That just an example of the powers they have.”

For transcript, audio and video: http://www.cfr.org/financial-markets/us-finance-hurting-growth/p37902

Stiglitz’s first comment from 35:45 minutes in.

Lucy’s question and Stiglitz’s answer from 39 minutes in.

GREECE’S ENDLESS LOOP OF DOOM – full version

GREECE’S ENDLESS LOOP OF DOOM – full version of New York Times op-ed

On 31st May 2016 the New York Times published the op-ed below (under a title that is unfortunate and not my choice). (For the NYT site, click here.) The version below is the original and contained graphs and data that could not be fitted in the printed version. (You can also download a pdf of the full article here.)

Greece’s disappearance from the financial headlines since then has been seen as a sign that its economy has stabilized. Sadly, it has not.

Lest we forget, Greece had already endured years of austerity. By 2013, more than a third of Greeks were living below the poverty line. By 2014, government wages and pensions had been cut 12 times in four years.

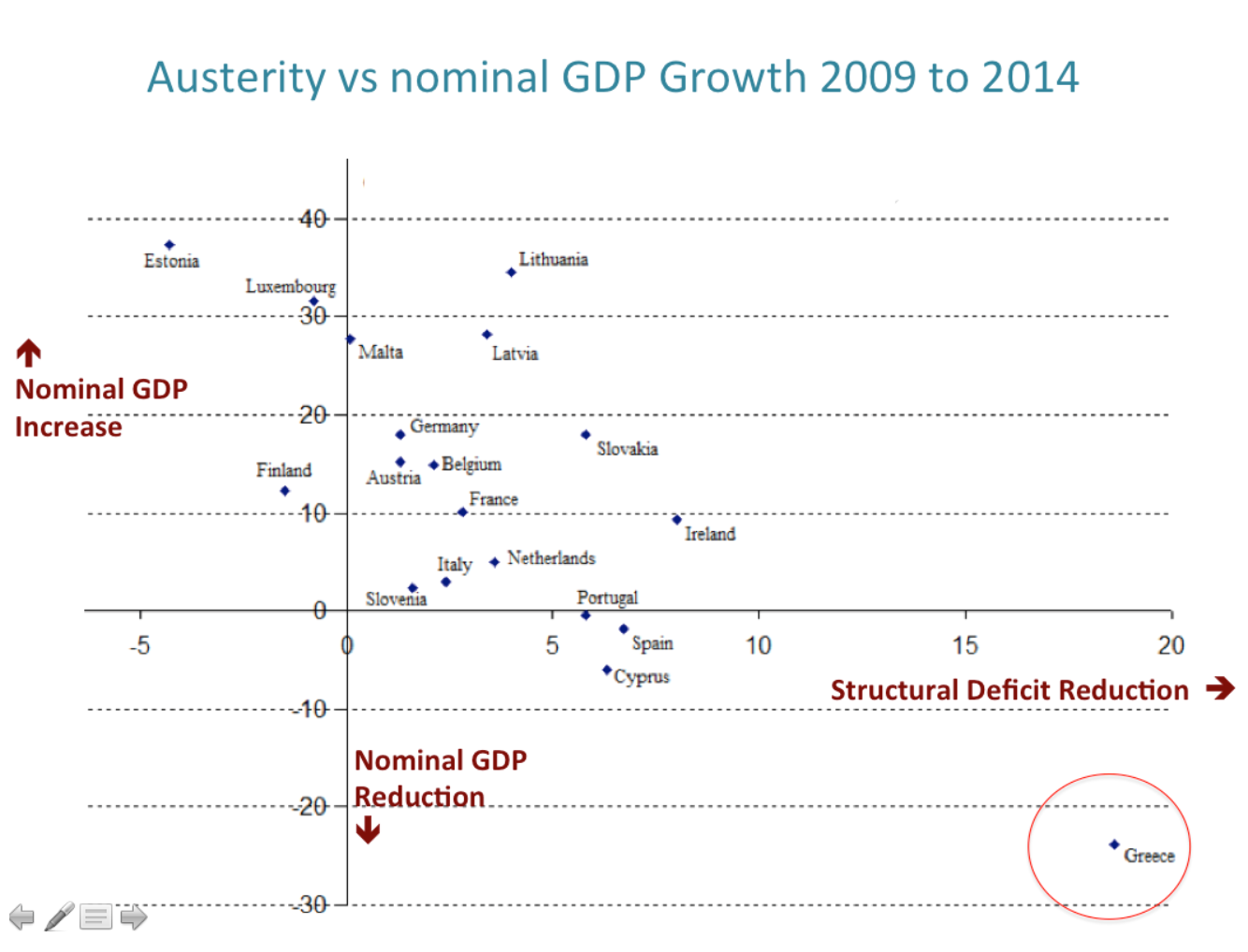

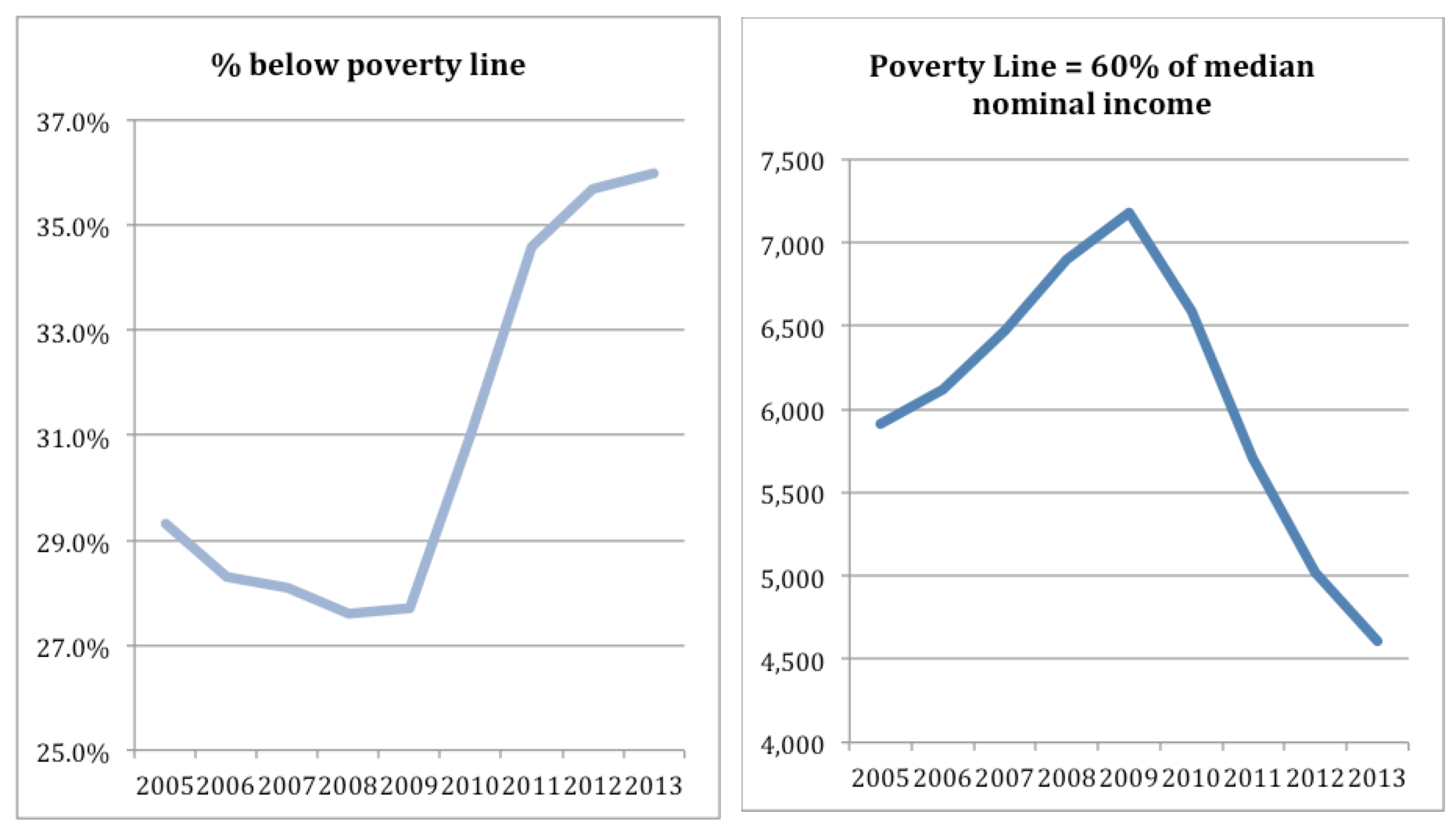

In comparative terms, Greece had absorbed austerity measures almost nine times the magnitude of those imposed in Italy and more than three times Portugal’s. The result? Between 2009 and 2014, Italy’s economy grew by a paltry 2 percent and Portugal’s contracted by 1 percent; in the same period, Greece’s national income dwindled by a catastrophic 26.6 percent — about the same as for America in the depths of the Great Depression (see Figure 1). The result was a humanitarian disaster only a latter-day John Steinbeck could adequately describe (Figure 2) for poverty data.

FIGURE 1 – Increase/Reduction in the structural deficit in percent of GDP terms versus nominal GDP growth/contraction. (Nb. A government’s budget deficit is computed as the difference between government expenditure and tax revenues as a percentage of national income. The structural deficit is computed in the same manner except that national income is estimated as the average of the nation’s income in the good and the bad years of the cycle.)

FIGURE 2 – The left hand side graph shows the percentage of the Greek population whose income falls below the official poverty line. The right hand side graph depicts the fluctuations of the official poverty line (which is conventionally drawn to equal 60 percent of median income). The combination of these two graphs reveals the extent of the humanitarian crisis: Between 2009 and 2013 (Nb. data for 2014 and 2015 is not in yet), the poverty line has fallen (along with median income) from €7,178 to €4,608. Despite this momentous drop, the percentage of the population that fell below that free-falling poverty line shot up from 27.7 percent to 36 percent. Moreover, this distressing trend has been continuing unabated for another three years (2014 to 2016), as the official data is bound to confirm.

Against this background, Greek voters elected my party, Syriza, in January 2015 to negotiate an end to self-defeating austerity in exchange for serious reforms. With the state now living within its means (i.e. new government expenditure was slightly lower than tax revenues), I strove, as the country’s new finance minister, to convince our European and institutional lenders that their interest and ours would best be served by reducing tax rates and avoiding further cuts to already much reduced pensions. As a compromise, I even promised a “deficit brake” — automatic tax hikes that would kick in if government revenues did not pick up within an agreed period.

Our sensible debt restructuring ideas and my deficit brake proposal fell on deaf ears, and I resigned. Greece’s creditors insisted instead on even higher sales taxes, as well as new cuts in pensions and wages. The Greek government’s capitulation to the creditors even involved a preposterous obligation that all Greek companies should pay, immediately and in full, their estimated tax for the next year. The cruel screw of austerity turned again.

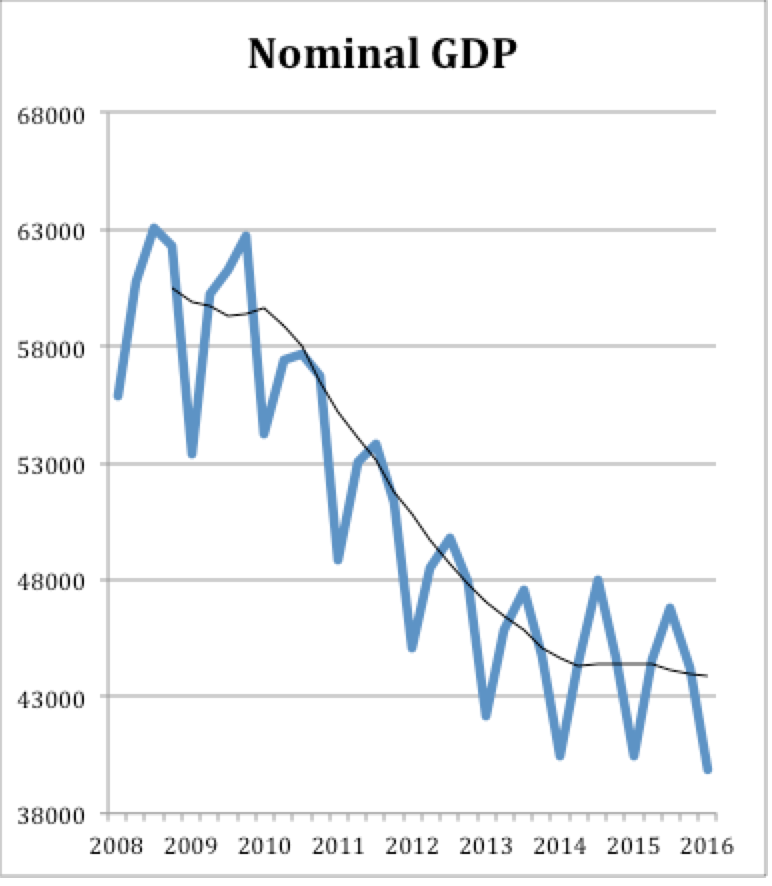

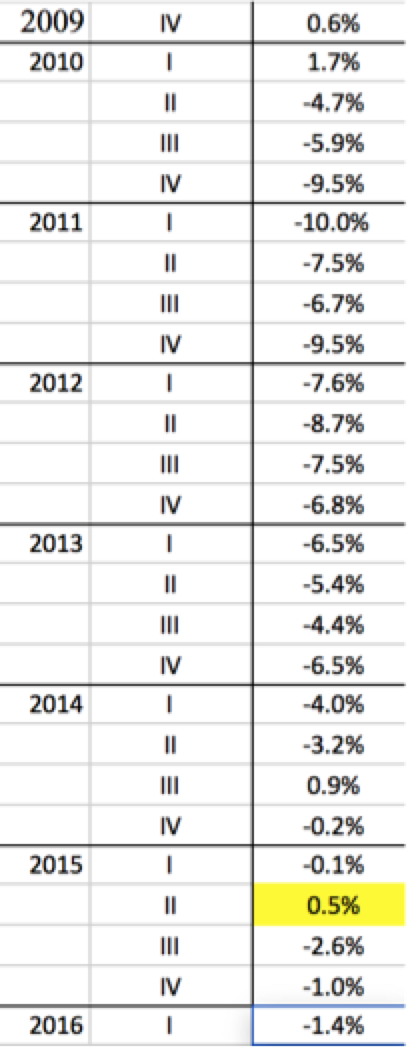

Once the new measures were implemented, incomes in Greece, which had picked up slightly while we put austerity on hold, began to fall again. (Figure 3 demonstrates that, indeed, the second quarter of 2015, when austerity was on hold, was the only quarter since 2008 of positive nominal income growth.)

FIGURE 3 – On the right, seasonally unadjusted quarterly (annualized) nominal GDP growth (Nb. Note that 2015Q2 was the only quarter of positive nominal income change. On the left, the downward path of nominal GDP in absolute numbers (GDP measured in market prices).

But the bank closures that were forced by Greece’s creditors to make our government yield, and the new austerity that followed, revived the recession (see, again, Figure 3). This increased the number of nonperforming loans on banks’ balance sheets — up to an astounding 45 percent of all loans — with the effect of denying credit to potentially profitable export-oriented firms. One in every two Greek families has no member earning a wage, while the cuts in public spending mean that for the past two years less than 10 percent of the jobless receive any unemployment benefit.

Behind the grim numbers, an ugly reality looms, one that gets uglier by the day. Small businesses have been crushed by punitive taxes, and a wave of home foreclosures is on the horizon. Greece’s hospitals are running out of basic necessities, while our universities cannot even afford to provide toilet paper in their restrooms. In Athens, these days, only the soup kitchens can be said to be flourishing.

Amid this endless suffering, have any lessons been learned? It seems not.

Greece’s economic misery seemed set to provoke a new standoff recently — except that, this time, it was between the International Monetary Fund and the European Union’s Brussels-Berlin nexus. Chancellor Angela Merkel of Germany is reluctant to confess to the Bundestag that Greece’s bailout loans were always unsustainable. To maintain the fantasy that they will be repaid as planned under the terms of last year’s deal, Berlin has insisted on setting a ludicrous target for Greece’s budget surplus. (That target is 3.5 percent of gross domestic product every year from 2018 to 2029; that amount is roughly equivalent, as a percentage of G.D.P., to America’s military budget — but in Greece’s case, purely to service its foreign debt.)

The German condition, that the European Commission is echoing, amounts to imposing permanently escalating austerity on Greece. The I.M.F. protested, correctly, that there is no level of austerity that can achieve this target. Indeed, judging by its spokesman’s comments as well as conversations between members of its staff published by Wikileaks, the I.M.F. had embraced the exact surplus target that I was proposing last year as well as most of the debt restructuring ideas I had put forward together with Jeff Sachs and Larry Summers.

In past weeks, there were many indications that the fund was ready to insist on this mixture of debt relief and a lower surplus target, and so less austerity. Unfortunately, last Tuesday’s meeting of the so-called Eurogroup — an informal body of eurozone finance ministers together with officials from the European Central Bank and the I.M.F. — dashed these hopes. With the I.M.F.’s managing director, Christine Lagarde, notably absent, her stand-in capitulated to the Brussels-Berlin axis, postponing any prospect of debt relief until talks a year or two hence.

Earlier this month, Athens had obediently introduced a fresh round of tax hikes and pension cuts — the sales tax in Greece now stands at 24 percent. The I.M.F.’s view is that these measures will fail to attain the impossible surplus target. The fund is right about that, but the new solution it has condoned is as bizarre as it is counterproductive.

Instead of reducing the surplus target, the I.M.F.’s representative at the Eurogroup meeting, Mr. Poul Thomsen, consented to the extraordinary decision to retrieve from the trash basket of last year’s negotiations the deficit brake that I had proposed in exchange for an end to austerity. The idea is that if the 3.5 percent surplus target is missed — and it will be — then new tax increases and spending cuts will kick in automatically. So, the very instrument that I had proposed as a substitute for austerity will now become its supplement. The mechanism will merely accelerate Greece’s downward spiral of austerity and recession.

Reason demands an end to this loop of doom. All Greece needs is a realistic restructuring of its debt, a primary surplus target of no more than 1.5 percent of national income and continued reforms that target oligopolies in economic sectors like supermarkets and the energy sector, as well as inefficiency and corruption in public administration.

Instead, the odd principle of imposing the greatest austerity for Europe’s most depressed economy lives on, spreading new misery through Greece and needlessly holding back recovery in Europe’s monetary union.

Yanis Varoufakis, a former finance minister of Greece, is a professor of economics at the University of Athens, and a co-founder of the DiEM25, the Democracy in Europe Movement

Executive suicides scratch Switzerland's picture

Business

|

Executive suicides scratch Switzerland's picture perfect veneer

ZURICH/FRANKFURT

|

Wauthier had blamed pressure from the company's then chairman Josef Ackermann in a suicide note, although Ackermann was cleared in a subsequent investigation.

Acquaintances of Senn, 59, said he had been withdrawn since he was ousted from the company late last year, though few details of the circumstances that led to him shooting himself at his family home in the upmarket Alpine resort of Klosters have emerged.

Martin Naville, chief executive of the Swiss-American Chamber of Commerce, said the business circles where Senn and Wauthier once moved had been left shocked, pondering what could have been done to prevent the tragedies.

"The only thing you can do is to be more attentive to signs," Naville said.

He knew Senn, who was president of the chamber, as well as Wauthier, who had British-French dual citizenship. He also knew Carsten Schloter, the German-born head of telecoms group Swisscom, who took his life in 2013, and Alex Widmer, head of bank Julius Baer, who committed suicide in 2008.

Their deaths contrast with the picture postcard image of Switzerland as one of the world's wealthiest and most stable countries.

Switzerland's overall suicide rate is below the global average, roughly in line with countries such as Germany, according to the World Health Organisation.

Naville said he saw nothing in Swiss executive culture to explain the deaths. "Every case can be very different," he said. "Human beings are so complicated."

But others describe a generation of managers caught between highly demanding international investors and Switzerland's conservative traditions.

"If you fail, you are expected to excuse yourself from the conversation and drop any further ambitions. You're not expected to show your face again," said Susan Kish, a former UBS banker who has started a number of businesses, including an entrepreneurship network in Zurich.

PROXY FOR SWISS ECONOMY

Switzerland has been hit in the past few years by a slowing global economy and a strong franc currency that has hurt vital exports.

Zurich Insurance mirrors many of the challenges and is now in the throes of restructuring as it slashes thousands of jobs.

"Zurich (Insurance) is a proxy for the Swiss economy," said Stefan Michel of Swiss business school IMD.

"Switzerland is no longer an island," he said. "The pressure from global shareholders and regulators is increasing. Whenever I ask people in the financial sector how they feel, they answer: 'I am tired'."

Staid for most of its nearly 150 years, Zurich Insurance rose to prominence in the 1990s with a series of takeovers. But its fortunes turned in 2001, when the Sept. 11 attacks in the United States left it with heavy losses, while runaway expenses at its headquarters hit the bottom line – and shareholder trust.

It underwent an overhaul before Senn was appointed CEO of Zurich in 2010.

Its chairman from 2012, Josef Ackermann, formerly Deutsche Bank's CEO, was pushing management to abandon its conservative course, people familiar with the matter have told Reuters, and take more risks on its investments to bolster returns.

Ackermann resigned after Wauthier's suicide note suggested he had been driven into a corner by the chairman, who was later exonerated in an investigation.

Senn is remembered fondly by employees who spoke to Reuters as someone who knew staff by name and shook hands with everyone at meetings, regardless of rank.

But after a series of profit warnings and an aborted takeover attempt for British rival RSA (RSA.L), he was pressured out by the company's Dutch chairman Tom de Swaan last year.

Reinhard Sprenger, an author and management consultant who has advised top Swiss firms, said corporate setbacks, with the near collapse of bank UBS during the financial crisis and the bankruptcy of airline Swissair, have jolted the country.

"The Swiss were once supremely self confident ... that has changed and they have come back to earth."

The annual economic conference in the Swiss resort of Davos, one of the top gatherings for the world's policymakers and business leaders, has become shorthand for a new generation of driven managers who put their corporations above national interests, said James Breiding, author of a book on how Switzerland became successful.

"Like Japan, Switzerland had a strong sense of community and egalitarianism. In the last 20 years, we've seen the emergence, however, of the 'Davos man,'" he said.

"Those men that embraced the Davos scepter found themselves in an increasingly lonely club."

(Additional reporting by Michael Shields; Editing by Susan Fenton)

UK is most corrupt country in the world

UK is most corrupt country in the world, says mafia expert Roberto Saviano

'It’s not the bureaucracy, it’s not the police, it’s not the politics but what is corrupt is the financial capital'

|

|

|

|

Britain is the most corrupt country in the world,

according to journalist Roberto Saviano, who spent more than a decade

exposing the criminal dealings of the Italian Mafia.

Mr Saviano, who wrote the best-selling exposés Gomorrah and ZeroZeroZero, made the comments at the Hay Literary Festival.

The 36-year-old has been living under police protection since

publishing revelations about members of the Camorra, a powerful

Neapolitan branch of the mafia, in 2006.

He told an audience at Hay-on-Wye: “If I asked you what is

the most corrupt place on Earth you might tell me well it’s Afghanistan,

maybe Greece, Nigeria, the South of Italy and I will tell you it’s the

UK.

“It’s not the bureaucracy, it’s not the police, it’s not

the politics but what is corrupt is the financial capital. 90 per cent

of the owners of capital in London have their headquarters offshore.

“Jersey and the Cayman’s are the access gates to criminal

capital in Europe and the UK is the country that allows it. That is why

it is important why it is so crucial for me to be here today and to talk

to you because I want to tell you , this is about you, this is about

your life, this is about your government.”

Prime minister David Cameron

faced growing calls for the UK to reform the offshore tax havens

operating on its own Crown Dependencies and Overseas Territories, as Britain hosted an Anti-Corruption Summit earlier this month.

The UK ranked 10th in Transparency International’s Corruption Perceptions Index 2015, which measures the perceived levels of public sector corruption worldwide.

Mr Saviano also weighed in on the EU referendum debate,

arguing a vote to leave would make the UK even more exposed to the

organised crime.

He said: “Leaving the EU means allowing this to take place. It means

allowing the Qatari societies, the Mexican cartels, the Russian Mafia to

gain even more power and HSBC has paid £2 billion Euros in fines to the

US government, because it confessed that it had laundered money coming

from the cartels and the Iranian companies. We have proof, we have

evidence.”- More about:

- Roberto Saviano

- Corruption

- Hay Festival

mercoledì 1 giugno 2016

Graphic of the fraud of the London gold market

London Gold Market – An infographic hosted at BullionStar.com

To embed this infographic on your site, copy and past the code below

Iscriviti a:

Post (Atom)

Post in evidenza

The Great Taking - The Movie

David Webb exposes the system Central Bankers have in place to take everything from everyone Webb takes us on a 50-year journey of how the C...

-

Dimensione sociale, crisi finanziaria, sovranità nazionale: il nodo della BCE di Claudio Moffa - 14/11/2011 Fonte: claudiomoffa Articolo...

-

Nov. 5, 2010 Slain executive left no trail of financial irregularities, bank says BY CHRISTINA HALL FREE PRESS STAFF WRITER Th...

-

Chris Powell: Gold market manipulation update Submitted by cpowell on Wed, 2015-10-28 21:55. Section: Documentation By Chris Powell, ...