Secret Information Belonging To Clients Of Some Of World's Biggest Hedge Funds Exposed In Massive Ransomware Attack

Last

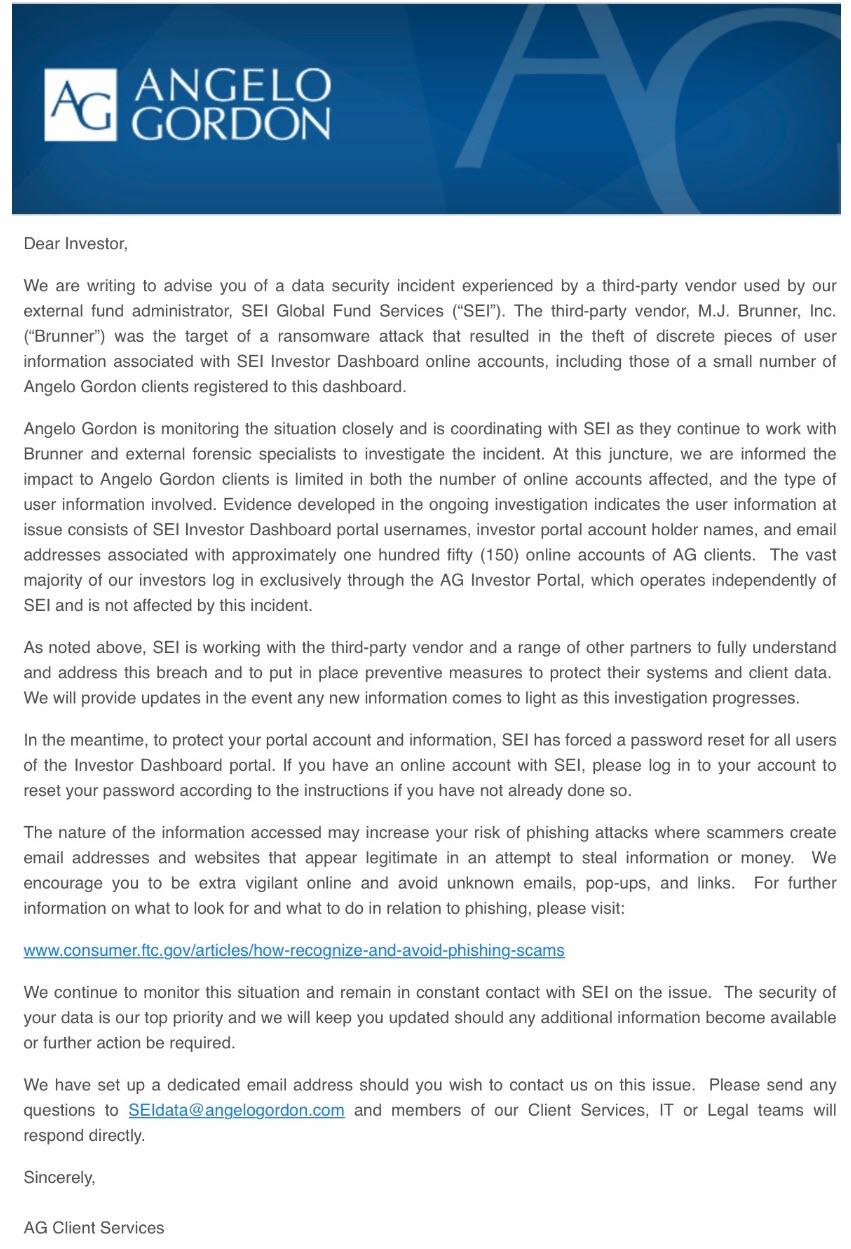

Thursday, investors in hedge fund Angelo Gordon received an unpleasant

letter advising them that a "data security incident" had taken place due

to a breach of a third-party vendor used by the fund's external fund

administrator, SEI Global Fund Services.

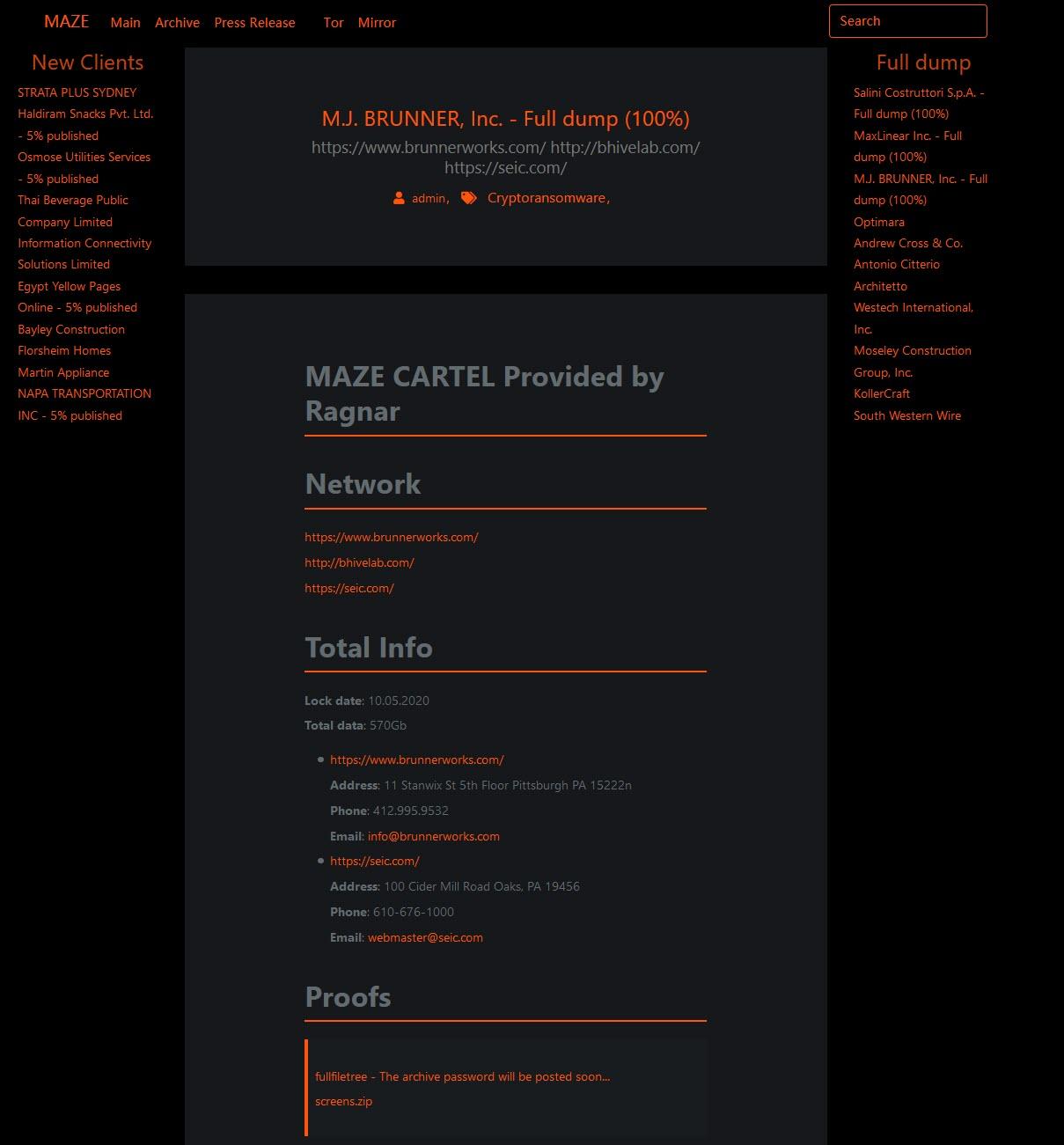

The hacked "third-party vendor" in question is M.J. Brunner, a

Pittsburgh- and Atlanta-based service provider that developed and

supports SEI's investment dashboard and online enrollment portal, was

the target of a ransomware attack that resulted in what the letter

described as theft of "discrete pieces of user information associated

with SEI Investor Dashboard online accounts."

And since countless other hedge funds also use the same fund

administrator, Dow Jones today reports that the hack attack also exposed

secret information belonging to clients of such iconic funds as Graham Capital, Fortress, Centerbridge and even PIMCO, demonstrating

again that all hackers need is to isolate the weakest link in any

security chain and all personal information becomes immediately exposed

for the world to see.

In this particular case, the unidentified hackers took files from

Brunner that contained user names and emails - and in some cases names,

physical addresses and phone numbers - associated with the dashboard.

The full data dump from the Ransomware attack, which has over 570GB in data, has been published online by a group called RagnarLocker at mazenews.top, a site historically linked with phishing attempts. The

compromised data includes everything from usernames and passwords, but

more importantly, SQL files that include live client data, including

positions, trades, and P&L statements.

The Oaks, Pa.-based SEI is a leading fund administrator that does

business with a broad swath of hedge funds and private-equity funds. As of June 30, SEI had $693 billion in client assets under administration and managed or advised on additional assets.

According to a Dow Jones report, Brunner was asked to pay a ransom

but declined, prompting the hackers to post company data obtained from

the May exfiltration online in July. Investors in funds like those SEI

counts as clients include pension funds, endowments and wealthy

individuals and families. Brunner told SEI about the attack in

late May, but weeks passed before SEI knew its clients' information had

been breached, people familiar with the matter said.

Curiously, there was also no mention of the devastating ransomware

attack during SEI's Wednesday earnings call; we hope the management team

issues an 8K addressing this minor "oversight." A spokeswoman for SEI

told Dow Jones that the company's network wasn't compromised and the

attack wasn't predicated on a vulnerability within its network.

"We take our clients' security very seriously, and we are working

with Brunner, the FBI and our impacted clients to understand the extent

to which SEI's or our clients' data has been exposed," she said.

A Brunner spokesman said in a statement its IT staff "detected, and

interrupted, a security incident involving some of our corporate systems

by an unauthorized actor. We immediately notified the FBI and will

continue to work with them through their investigation."

Meanwhile, in its letter, Angelo Gordon said it was monitoring the

situation closely and is coordinating with SEI as they continue to work

with Brunner and external forensic specialists to investigate the

incident.

At this juncture, we are informed the impact to Angelo Gordon clients

is limited in both the number of online accounts affected, and the type

of user information involved. Evidence developed in the ongoing

investigation indicates the user information at issue consists of SEI

Investor Dashboard portal usernames, investor portal account holder

names, and email addresses associated with approximately one hundred

fifty (150) online accounts of AG clients. The vast majority of our

investors log in exclusively through the AG Investor Portal, which

operates independently of SEI and is not affected by this incident.

In any case, we urge all clients of Angelo Gordon, as well as PIMCO,

Fortress, and any other fund that uses SEI as a manager, to promptly

change their log in credentials as their private data may well be in the

open.

The attack is the latest in a string of ransomware incidents that

have affected the financial-services sector through its far less secure

suppliers. According to DJ, this past March financial-technology

provider Finastra suffered an attack that forced it to temporarily take

its systems offline. An attack on Finablr's foreign-exchange business

Travelex in late December shut down its website for weeks, which had a

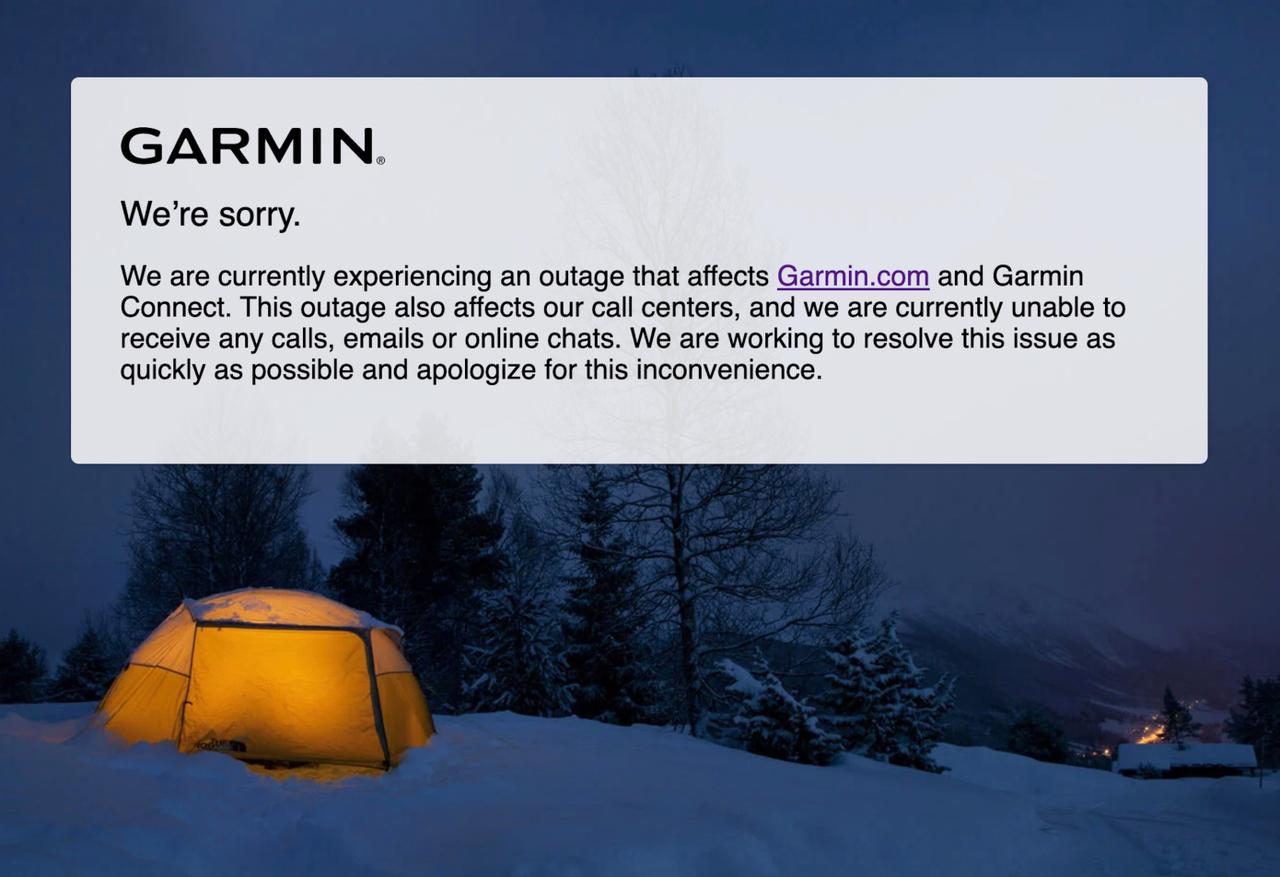

knock-on effect on banks that use its services. Garmin's user data -

which includes highly confidential personal health information - are

currently locked out due to a suspected ransomware attack.

Officials from the National Security Agency have warned that vendors

and service providers have emerged as popular targets, as successful

attacks can yield access to large amounts of sensitive information for a

web of clients, or even systems access.

There is a school of though which believes that International Finance

with its preponderant Jewish interest and the Monetary System under

which most of the

world has suffered from mass unemployment was doomed

to be superseded by Hitler’s credit system based upon a

goods standard and international barter. This would displace gold, the

tool of the Internationalists.

I believe this myself.

But some go so far as to say that the war was brought

about so that, if Hitler could be defeated, the Gold Standard Monetary

System, which is fraudulent, could be maintained to the benefit of Wall

Street and other large Gold

Controllers.

I do not believe that.

It might be worth a war from the point of view of

Wall Street, but it would not be worth this war. This

war shows every trace of our having been dragged into

it blindfolded and uneprapared. Wall Street would not

have allowed that. Wall Street knows that if the Germans won the war, there would be no more Wall Street.

In my opinion there was more to it than the survival

of the fraudulent Gold Standard System. The necessities

of racial survival made it urgent for the Jews to act without delay. Their considerable influence in Wall Street

together with other participants in the spoils of the fraudulent system made it not too difficult to get the “Street”

to support a war which was represented as inevitable.

This is not the place to go into the intracacies of

monetary systems. The kernel of the problem is that

credit based upon gold is insufficient for the needs of

modern commerce. A short supply of money and credit

is best for the usurer or money-lender, since scarcity raises

the rate of interest borrowers must pay. Power to regulate the amount of money and credit available enables

the controllers of Gold to dominate world affairs, economically and politically. The creation of inextinguishable

national debts is part of the system of control and with

control goes domination. This system of economic and

financial bondage was doomed by the expansion of the

barter system developed by National Socialist Germany.

(For a more detailed explanation see the chapter, The

Peace We Lost in A PEOPLE’S RUNNYMEDE, by Robert Scrutton, Andrew Dakers, publisher.)

FOX Business’ Charlie Gasparino on Barclays’ and Deutsche Bank’s potential involvement with Jeffrey Epstein.

The New York Times on

Monday named multiple Deutsche Bank executives who were responsible for

the bank’s relationship with Jeffrey Epstein, the convicted

sex offender and financier who was found dead by apparent suicide last

August.

This comes one week after New York state’s Department of Financial Services

fined Deutsche Bank $150 million “for significant compliance failures

in connection with the Bank’s relationship with Jeffrey Epstein.”

Deutsche

Bank confirmed to FOX Business that The New York Times piece is

accurate, and said that all individuals involved have been appropriately

disciplined.

A

spokesman for Deutsche Bank said the 2015 arrival of Jan Ford, the

bank’s head of compliance in the Americas, was a turning point that

ultimately led to the termination of the bank’s relationship with

Epstein.

Deutsche

Bank maintained a relationship with Epstein from August 2013 until

December 2018 despite the fact that he was convicted of soliciting

prostitution from a minor in 2008, according to a consent order filed by New York financial regulators.

The

Times reports that Paul Morris, who previously helped manage Epstein’s

account at JPMorgan, was the banker that originally introduced Epstein

to bank executives in 2013 as a client who could generate $2-4 million

of revenue annually. He was referred to as “RELATIONSHIP MANAGER-1” by

financial regulators in the consent order.

It

was Charles Packard, the head of the bank’s American wealth-management

division, who approved of the bank’s relationship with Epstein in 2013,

according to The Times.Both Morris and Packard are no longer employed at Deutsche Bank.

After

the relationship with Epstein began, Deutsche Bank ignored dozens of

red flags that regulators say should have prompted additional scrutiny.

According to a press release

by the NY Department of Financial Services, these red flags included:

“payments to individuals who were publicly alleged to have been Mr.

Epstein’s co-conspirators in sexually abusing young women; settlement

payments totaling over $7 million, as well as dozens of payments to law

firms totaling over $6 million for what appear to have been the legal

expenses of Mr. Epstein and his co-conspirators; payments to Russian

models, payments for women’s school tuition, hotel and rent expenses,

and (consistent with public allegations of prior wrongdoing) payments

directly to numerous women with Eastern European surnames; and periodic

suspicious cash withdrawals — in total, more than $800,000 over

approximately four years. “

The New York Times details how Morris

and Packard visited Epstein at his Manhattan mansion in January 2015 to

ask him about these red flags as well as “about the veracity of the

recent allegations” in the media. They left satisfied with Epstein’s

explanation.

Deutsche Bank ended its relationship with Epstein in November 2018 after The Miami Heraldexposed the extent of Epstein’s sexual misconduct as well as the sweetheart deal he got from prosecutors.

Dieter Wemmer is capping an illustrious finance career with a

seat on UBS' board. He is also partnering with a fearsome hedge fund –

which may soon roil the financial industry.

In the Netherlands, the mention of Elliot Management is synonymous

with unwelcome activism: the U.S.-based hedge fund in 2017 attempted to

force AkzoNobel into an unwanted merger with American PPG Industries.

The warring factions buried the hatchet – via a lengthy court battle.

Elliott has a new target: it snapped up three percent of the

largest Dutch insurer NN in February. Last month, Elliott called for NN

to cut costs and to boost cash flow by taking more risk in its bond

portfolio, in a website devoted to the campaign dubbed «the time is now».

Missed Out On CEO Job

Led by Paul Singer, Elliott has marshaled influential support for its efforts – Dieter Wemmer supports the U.S. hedge fund, and also bought a small stake in NN. «There

are ways to generate higher investment returns without taking on

unusual risks,» the German-Swiss executive told Dutch daily «NRC Handelsblad»(in Dutch) last month.

Wemmer and the activist fund are a surprising match, and a coup for

Elliott: the 63-year-old looks back on a distinguished executive career

in the insurance industry. He worked his way up to finance chief of

Swiss insurer Zurich, where he was a leading contender to replace

then-CEO James Schiro. Zurich's board in 2010 picked Martin Senn instead – a five-year tenure that ended quietly in 2015 (Senn died by suicide six months later).

Lauded As Manager

Wemmer, a Cologne native, had moved to Allianz as their finance chief

in 2011, a role he inhabited until reaching retirement age three years

ago. He had in 2016 been elected to UBS' board, where he is a member of

the governance and nomination committee (as well as audit and pay

bodies).

The Rhinelander's career enshrined him into Europe's financial

establishment, and Wemmer is also highly thought of both because he is

sharp as a tack (he has a Ph.D. in mathematics) and because he is an

excellent manager. In 2012, he was elected Swiss blue-chip finance boss

of the year by CFO Forum. Those who have worked for Wemmer, who didn't respond to a request for comment about his plans with Elliott, speak glowingly of him.

Activist Efforts Bear Fruit

Wemmer signaled a conciliatory stance in his comments to «NRC

Handelsblad» about NN: «The team can either listen to us or ignore us

(...) we trust the company and the management.» Given Elliott's 70-slide

barrage, Wemmer sounds like he has been assigned the good guy role in a

good cop, bad cop strategy.

Elliott's efforts bore fruit: NN, led by David Knibbe, is

dropping its initial resistance and dipping into somewhat riskier

investments, which should lift free cash flow. The insurer last month

promised to keep raising its dividend yearly.

Next Bank Chairman?

The concession paves the way for the kerfuffle to calm down – and

what of Wemmer? In Switzerland, he is touted as a candidate to preside

either UBS or Credit Suisse, where both banks are seeking a new

chairman.

At Credit Suisse, Chairman Urs Rohner is in

the twilight of his a ten-year tenure overseeing the Swiss bank – a stay

beyond April of next year would likely reignite a power play with the

bank's biggest shareholder. At UBS, Axel Weber is scheduled to hand over the reins in the boardroom by 2022.

Small Finance World

UBS' succession search could be complicated by the bank's domestic head, Axel Lehmann. The

Swiss banker and insurance executive knows Wemmer: the duo worked

side-by-side at Zurich Insurance as top finance and risk executives.

Like Wemmer, the 60-year-old Lehmann was also passed over for the CEO

role at Zurich. A further small-world quirk: incoming UBS boss Ralph Hamers was

responsible for NN in its current form. It was the Dutch banker's

decision to spin off the former Nationale-Nederlanden in 2014, severing

ties entirely four years ago.