The Swiss referendum system has proved to be a useful incubator of radical economic ideas. Two years ago, a proposal was unsuccessfully put to voters

to introduce a generous universal basic income. And next week, the

Swiss will vote on a proposal that, if passed, would transform the

economy even more radically than UBI would have done.

The so-called “Vollgeld” or “sovereign money” initiative — covered at length

by my colleague Ralph Atkins — aims to require private banks to back

clients’ deposits fully with central bank reserves. Put differently,

they would abolish the fractional reserve banking practised virtually

everywhere, under which private banks can create deposits when they

issue loans over and above the cash, currency and reserves with the

central bank that they possess in assets.

The Vollgeld promoters

are right about two big things. The first is that in a fractional

reserve system, the amount of money circulating in an economy is largely

determined by private banks and their decentralised, profit-maximising

decisions about how much to lend. The broad money supply consists almost

wholly of bank deposits created ex nihilo by private

institutions, rather than government-issued money. Just making more

people realise this is itself a benefit of the referendum campaign.

(Free Lunch has described this phenomenon in our analysis of the Bank of England paper that remains the best explanation of how money is created by banks.)

The

second is that if we had to design a system for managing the economy’s

money supply from scratch we would never opt for what we have today. A

stable and appropriate size of the money supply is a deeply important

public good. It is a public good in the general sense that the

government is rightly held responsible for it; but it is also a public

good in the technical economic sense in that it has properties which

mean it will not be adequately provided by privatised free markets.

Suffice to note that profit-maximising private banks have an incentive

to expand lending when money supply growth is already too high and

retrench when monetary stimulus is most needed. In other words, they

create credit cycles. They also have no incentive to take into account

the effect their money creation has on others.

Full reserve

backing — essentially nationalising the money supply — must in principle

be superior, at the very least because it would give central banks more

tools to manage the economy. Central banks today determine the amount

of “base money” (cash and central bank reserves) but have no direct

control over “broad money” — what we use to pay for goods and services

in real economic transactions. Having such control would allow them to

both keep doing what they do at the moment (target interest rates or

using more unconventional tools such as securities buying) and to try

bolder monetary instruments such as directly managing the amount of

broad money in circulation or issuing “helicopter money”.

And in a crisis, banks would no longer be endangered by deposit runs,

since deposits would be fully backed by the central bank.

The

Vollgeld initiative is thus of a piece with earlier considered proposals

for comprehensive reform of the fractional reserve system, such as John

Kay’s call for narrow banking or Lawrence Kotlikoff’s proposal for what he calls limited purpose banking.

These

considerations do not by themselves seal the case for reform. But they

do mean that the burden of proof is on those who oppose the change. So

far they have not fully shouldered it. (Those behind the initiative

may have over-reached, however, because their proposal seems not only

to require full-reserve banking but also provide for direct monetary

financing of the government and state control of credit allocation.

These are conceptually distinct from full-reserve banking and should be

decided separately.)

The head of the Swiss central bank, Thomas Jordan, has come out strongly against the proposal

saying it “would hurt Switzerland”. Some of his chief arguments,

however, are contradictory. On the one hand, he argues that full reserve

backing would interfere with banks’ ability to lend, they could only

lend out funds deposited with it for such purposes, rather than as

liquid deposits. Such “maturity transformation” — funding long-term

loans with deposits redeemable at short notice — is the essence of

banking. Jordan rightly says that if the initiative passes, banks would

instead have to solicit funds on the understanding that they would be

used for long-term loans.

At the same time, however, he argues

that savers would be hurt because reserve-backed deposits would be less

well-remunerated. But the latter is precisely what would attract savers

to fund the former. If they do so with greater understanding of the

risk, that should make for better market pricing of credit. And maturity

transformation would not end, banks would just look more like mutual

funds whose investors may withdraw money on short notice so long as not

too many others try the same.

What is clear is that full reserve

requirements would hurt the current business model of banks. But that

cannot be an argument against a reform that is otherwise in the public

interest.

My comment below:

Marco SabaDear

Martin, what we have to understand is that you can't have a bank run on

digital money if this money is recognized for what it should be: CASH.

Banks deposits are yet recognized as CASH by international accounting

rules on cash flows (IAS-IFRS 7.6 and US-GAAP ASC 305-10-55-1 : *Cash on

deposit at a financial institution shall be considered by the depositor

as cash rather than as an amount owed to the depositor."). The problem

occurred when the banks were pretending that deposits are not CASH just

for themselfs, but by blockchaining the system of money creation what I

say may become self-evident.

How tough can life really be at the top of a ‘Big Four’ auditing firm? You inhabit a world where not only must customers by law buy your product, but, happily, one where the most lucrative also seem wedded to dealing with only the biggest practices — whether out of snobbery, the need for international audit coverage, or just the nebulous sense that investors might otherwise disapprove.

The one nightmare you have is that a giant accounting scandal could somehow bring retribution. Your size and reach makes you a tempting target. But even here, that same oligopoly rides faithfully to the rescue. Since the demise of Arthur Andersen — the fifth pillar of what was until 2002 the big five accountants — the authorities have helpfully thrown a cordon sanitaire around the survivors, fearing the descent into an even more dominant big three.

It is why when KPMG was found to be peddling illegal tax schemes in the US in 2005, it was let off with no more than a slap on the wrist by the authorities. Or why the whole big four — PwC, EY, KPMG and Deloitte — emerged from the furnace of the financial crisis with just a minor singeing.

There is, however, one nagging blot on this landscape. Each successive scandal raises the same awkward questions. Does this comfortable structure really promote audit quality? And by allowing a few giant firms to dominate the profession; has control of this systemically important industry been handed to a few self-interested actors — concerned mainly with preserving their own privileges rather than promoting the public good?

The collapse of the British outsourcing firm Carillion is the latest scandal to cause these worries. Despite absorbing expensive advice and assistance from all of the big four at a princely cost of £51m over a decade, its failure has been dominated by allegations of financial misreporting. How did the auditors, the giant KPMG, express no concern over reported profits of £150m just months before it emerged these were illusory?

Last week’s parliamentary report into the scandal called for a break-up of the big four, saying they operated as a “cosy club incapable of providing the degree of independent challenge” that was required.

It is hard to argue that some sort of shock is needed. Markets only function when participants perceive some threat to their position if they fail to perform or innovate. Yet in auditing, the moat between the big four and the rest is only widening, despite recent moves designed to reduce conflicts and spark more rivalry. Brought in after the crisis, these oblige quoted companies periodically to re-tender audits.

In March, Britain’s fifth-biggest firm, Grant Thornton, announced it would no longer tender for audits of FTSE 350 companies. It said that all retendered contracts were simply being passed reflexively around the big four.

Add to all that the regulator’s well-known “light touch” approach to the top firms, and you have a situation where big four partners may no longer feel they have to look over their shoulders. That makes them vulnerable to the blandishments of a high-paying client, whose boss has a life-changing bonus riding on its next figures, and some daring calculations to push. Rather than holding themselves and clients to the most exacting standards, the oligopolists can use their influence to shrug off liability, introduce overly complex disclosures and procedures that need heavy investment, and find ways to introduce “tick box” formulas into what should be principled rules.

Would break-ups change all this? Potentially yes, if investors were also prepared to step up and be both more demanding of audits, and rewarding of quality. The present arrangement, in which the company chooses the supplier of the audit rather than the (passive) investor, is unhealthy, leading to the sort of conflicts which bedevil, say, the US health insurance market.

The practical challenges are not insuperable. The big four claim theirs is a special market that needs scale because of the global demands. But there is little difference to legal services. And there are plenty of international law firms. Nor is it impossible for Britain to act unilaterally. The big four are global alliances built on national partnerships. Britain could catalyse wider action by leading the way.

There is a public interest in making life less comfortable for the masters of the auditing universe; not least to restore sterner oversight to those that perform this vital function. When asked in the 1930s who audited the auditors, Arthur Carter, a partner at the US firm Haskins & Sells responded: “Our conscience.” That was queasy then. It should not be acceptable now.

jonathan.ford@ft.com

Letter in response to this column:

Buy cover for balance sheets / From Thomas Abraham

Dear Supporter of the Swiss Sovereign Money Initiative,

The 10th June, the

date of the national referendum on Sovereign Money in Switzerland, is

coming up fast. The ballot papers have been sent out, and the campaign

is being hotly discussed and debated all over Switzerland.

The sovereign money initiative was debated in the Arena TV show (in

Swiss German, German subtitles) on the main Swiss TV sender SRF. Our

speakers were excellent, as was the moderator and most of the SRF

mini-cartoons about how the money system works and would work under a

sovereign money system. The opposition - politicians and economists -

did not appear to have a good technical knowledge (though they mentioned

"risky experiment" many times).

Swiss newspapers large and small have been writing about the sovereign

money initiative extensively - mostly explaining it fairly well -

although those against it focus on it being an experiment and driven

from abroad with foreign money (not true: despite trying hard to get

some foreign millions, I failed).

Here are some links to articles and blogs in English:

Fiat Money: Swissy fit

FT Lex column (paywall) 5/5/18 - makes good point why Thomas Jordan

(SNB chair) is opposed: "central bankers would shoulder increased blame

for any economic woes"

The international conference on sovereign money "Our Money, Our Banks, Our Country" held in February reported on in a previous newsletter is now available in its entirety online.

Arguments of our opponents - and our rebuttals

In summary - our opponents are running a fear campaign: the main

argument they are using is that the sovereign money initiative is an

unnecessary experiment. This shows they have found no valid technical

arguments against it. There is now a "No to sovereign money" website.

This "No" campaign has kicked-off with posters going up all over the

place - they clearly have much more funding than we do.

Detailed arguments from different organisations:

1) From the government and parliament:

In a Swiss people's initiative which comes to referendum, the Swiss

Federal Council and parliaments can give their recommendations. The

Council of States voted 42 to zero against the sovereign money

initiative, with one abstention. The National Council voted 169 to 9

against, with one abstention. The Federal Council also recommends voting

against the initiative. The main arguments together with our answers

(in italics) in brief, are:

A sovereign money system cannot guarantee financial stability - the aim of the initiative is to make people's money safe (we can't prevent a global financial crisis affecting Switzerland)

It hasn't been tried in any other country -

it's not new, it's what happened when banks were prevented from

printing their own banknotes and the Swiss National Bank was founded

It would be a radical change from the well-functioning system we have now -

the system we have now is not functioning, debt is mushrooming and all

experts agree it is not "if" we have another financial crisis, but

"when"

It would weaken the Swiss financial sector, to the disadvantage of banks' customers - having a totally secure money will be an advantage for Swiss wealth management and banks' customers

It would give too much power to the Swiss National Bank which would put it under political pressure - Do

we really want the power of money creation to be in the hands of

private profit-motivated businesses? The SNB already copes with

political pressure - it must act in the best interests of Switzerland

Measures have already been taken to strengthen financial stability - We know big banks are already planning to get round the new Basel rules

There are several mistakes in the official booklet sent to all voters, the main one being that under the sovereign money system all money

must enter the economy debt-free. This is incorrect: as well as new

money being spent into the economy debt-free, money can be lent into the

economy as banks may borrow money from the Swiss National Bank. (This

means a 'credit crunch' could only occur if the SNB chose not to lend

money to banks at reasonable rates). A legal process against the state

for providing incorrect information is underway.

Thomas Jordan, Chair of the SNB, has come out strongly against the

sovereign money initiative saying "sovereign money is an unnecessary and

dangerous experiment, which would inflict great damage on our country".

However, he appears not to have understood the sovereign money

initiative as he wrongly claims that it would force the SNB into

following a policy of targeting the money supply rather than interest

rates. There is nothing to stop the SNB from targeting interest rates

under the sovereign money system which it can do by setting the interest

rates at which it is willing to lend to banks.

Here are documents and speeches from the SNB against the sovereign money initiative.

Thomas Jordan's January speech has been critiqued by Ralph Musgrave, a supporter of ours.

3) From the Swiss Bankers Association

The Swiss Bankers Association commissioned Prof Bacchetta to write a study against

the sovereign money initiative. This has the guise of being a

scientific report, but is absolutely full of fundamental errors and

devious statistical handling (e.g. choosing the optimum time period for

interest rates to give the worst possible outcome of the effect of

sovereign money on the economy, the result being 0.4% less growth). This

has been strongly critiqued in a 85-page report by Christian Gomez, and also in a report by Ralph Musgrave.

4) Political Parties

All political parties are against the initiative except for the Green

Party who are neither supportive nor against and give a "free vote". The

parties who are against have come together in the "Vollgeld-Nein" (No to sovereign money) group, who are focusing on the fear campaign of "risky, expensive and damaging".

Results of the polls

Despite the well funded "No" campaign supported by the government,

parliament, the SNB and all political parties except the Green Party,

polls show we are still in the running but the "No" side is in the lead.

Note: if you click on the links below to see the German reports with

charts, be aware that there are two totally unrelated votes on 10th

June: the sovereign money initiative ("Vollgeld") and "Geldspielgesetzt"

(to do with online gambling). In both reports the "Geldspielgesetzt"

comes first, and you must scroll down to get the results for "Vollgeld".

1) The most recent poll (mid

May) shows 39% of respondents plan to vote for (or probably vote for)

the sovereign money initiative, with 54% planning to vote against (or

probably vote against) the initiative. (These results are collected

through an internet link).

There is a breakdown by political party, language-region, gender

and age. The people who support the vote are then asked which

(supportive) arguments they most agree with, and the people against the

vote are asked which (opposition) arguments they most agree with.

Parties: Green Party - For; Social Democratic Party (left wing) - Undecided; all others - Against

Language-region: German - Against; French - Undecided; Italian - Undecided

Age: Under 35 - Against; 35-49 - Against (only just); 50-64 - Undecided; Over 65 - Against

60% of those against the

initiative agreed with the statement "Our monetary and currency system

is working. A radical change to it would be an adventure with

incalculable risks" as the main reason to be against.

34% of those for the initiative agreed with the statement "In

the event of a banking crisis, our bank deposits are not secure because

they are virtual book money" and 31% with "The profits of money creation

should benefit the general public" as their main reason to be for.

59% of respondents would like the Swiss National Bank to create Swiss francs, and

62% think that private banks being allowed to create money leads to higher chances of financial bubbles.

Despite

this, only 35% plan to vote for (or probably vote for) the sovereign

money initiative, with 49% planning to vote against (or probably vote

against) the initiative (German speakers).

Their prognosis is that the numbers voting for people's initiatives tend

to drop over time, unless there is some significant event that

influences people otherwise. (The results were collected by telephone).

There is a breakdown by political party and language-regions:

Parties: FDP (Centre right) - strongly Against; all others - undecided.

(Interestingly the SPV (right wing) show a similar voting profile to the

left wing Social Democrats despite the SVP leadership being strongly

against).

Language - the French and Italian regions are much more supportive than the German-speaking region:

German-speaking region: 35% For, 49% Against

French-speaking region: 42% For, 27% Against

Italian-speaking region: 45% For, 36% Against

A big Thank You to

all of you who have made generous donations. Our campaign is now

focussed on social media and small-scale advertising, for example in

buses and trams. If you would like to donate you can do it using PayPalor

by transferring money to our Postfinance account: Vollgeld-Initiative,

Postfinance 60-354546-4, BIC POFICHBEXXX , IBAN CH61 0900 0000 6035 4546

4

If

you know any Swiss people, now is the time to get in touch and tell

them why you would like them to support the sovereign money initiative

(German: Vollgeld-Initiative, French: l’initiative Monnaie Pleine,

Italian: Iniziativa Moneta intera).

By the way: the results of the referendum will be out on the afternoon of 10th June.

There’s one incredible feature of cryptocurrencies that almost everyone seems to have missed, including Satoshi himself.

But it’s there, hidden away, steadily gathering power like a hurricane far out to sea that’s sweeping towards the shore.

It’s a stealth feature, one that hasn’t activated yet.

But when it does it will ripple across the entire world, remaking every aspect of society.

To understand why, you just have to understand a little about the history of money.

The Ascent of Money

Money is power.

Nobody

knew this better than the kings of the ancient world. That’s why they

gave themselves an absolute monopoly on minting moolah.

They

turned shiny metal into coins, paid their soldiers and their soldiers

bought things at local stores. The king then sent their soldiers to the

merchants with a simple message:

“Pay your taxes in this coin or we’ll kill you.”

That’s

almost the entire history of money in one paragraph. Coercion and

control of the supply with violence, aka the “violence hack.” The one

hack to rule them all.

When

power passed from monarchs to nation-states, distributing power from

one strongman to a small group of strongmen, the power to print money

passed to the state. Anyone who tried to create their own money got

crushed.

The reason is simple:

Centralized

enemies are easy to destroy with a “decapitation attack.” Cut off the

head of the snake and that’s the end of anyone who would dare challenge

the power of the state and its divine right to create coins.

That’s what happened to e-gold

in 2008, one of the first attempts to create an alternative currency.

Launched in 1996, by 2004 it had over a million accounts and at its peak

in 2008 it was processing over $2 billion dollars worth of

transactions.

The

US government attacked the four leaders of the system, bringing charges

against them for money laundering and running an “unlicensed money

transmitting” business in the case “UNITED STATES of America v. E-GOLD, LTD, et al.”

It destroyed the company by bankrupting the founders. Even with light

sentences for the ring leaders, it was game over. Although the

government didn’t technically shut down e-gold, practically it was

finished. “Unlicensed” is the key word in their attack.

The power to grant a license is monopoly power.

E-gold was free to apply for interstate money transmitting licenses.

It’s just they were never going to get them.

And of course that put them out of business. It’s a living, breathing Catch-22. And it works every time.

Kings and nation states know the real golden rule:

Control the money and you control the world.

And so it’s gone for thousands and thousands of years. The very first emperor of China, Qin Shi Huang

(260–210 BC), abolished all other forms of local currency and

introduced a uniform copper coin. That’s been the blueprint ever since.

Eradicate alternative coins, create one coin to rule them all and use

brutality and blood to keep that power at all costs.

In the end, every system is vulnerable to violence.

Well, almost every one.

The Hydra

In

decentralized systems, there is no head of the snake. Decentralized

systems are a hydra. Cut off one head and two more pop-in to take its

place.

In 2008, an anonymous programmer, working in secret, figured out the solution to the violence hack once and for all when he wrote:

“Governments are good at cutting off the heads of centrally controlled

networks like Napster, but pure P2P networks like Gnutella and Tor seem

to be holding their own.”

And the first decentralized system of money was born:

Bitcoin.

It was explicitly designed to resist coercion and control by centralized powers.

Satoshi

wisely remained anonymous for that very reason. He knew they would come

after him because he was the symbolic head of Bitcoin.

That’s

what’s happened every time someone has come forward claiming to be

Satoshi or when someone has been “outed” by the news media as Bitcoin’s

mysterious creator. When fake Satoshi Craig Wright came out, Australian

authorities immediately raided his house. The official reason is always spurious. The real reason is to cut off the head of the snake.

As

Bitcoin rises in value, the hunt for Satoshi will only intensify. He

controls at least a million coins that have never moved from his

original wallets. If VC Chris Dixon is right and Bitcoin rocket to $100,000 a coin,

those million coins will shoot up to $100 billion. If it goes even

higher, say a $1 million a coin, that would make him the world’s first

trillionaire. And that will only bring the hammer down harder and faster

on him. You can be 100% sure that black ops units would be gunning for

him around the clock.

Wherever he is, my advice to Satoshi is this:

Stay anonymous until your death bed.

But

resistance to censorship and violence are only one of a number of

incredible features of Bitcoin. Many of those key components are already

at work in a number of other cryptocurrencies and decentralized app

projects, most notably blockchains.

Blockchains

are distributed ledgers, the third entry in the world’s first

triple-entry accounting system. And breakthroughs in accounting have

always presaged a massive uptick in human complexity and economic

growth, as I laid out in my article Why Everyone Missed the Most Important Invention in the Last 500 Years.

But

even triple-entry accounting, decentralization and resistance to the

violence hack are not the true power of cryptocurrencies. Those are

merely the mechanisms of the system, the way it survives and thrives,

bringing new capabilities to the human race.

The ultimate feature is one that Bitcoin and current cryptocurrencies have only hinted at so far, a latent feature.

The true power of cryptocurrencies is the power to print and distribute money without a central power.

Maybe that seems obvious, but I assure you, it’s not. Especially the second part.

That power has always rested with the divine right of kings and nation-states.

Until now.

Now that right returns to its rightful owners: The people.

And that will blow open the doors of world commerce, sowing the seeds for Star Trek like abundance economics, leaving the Old World Order of pure scarcity economics in the pages of history books.

There’s just one problem.

Nobody has created the cryptocurrency we actually need just yet.

You see, Satoshi understood the first part of the maxim, the power to print money. What he missed was the power to distribute that money.

The

second part is actually the most crucial part of the puzzle. Missing it

created a critical flaw in the Bitcoin ecosystem. Instead of

distributing the money far and wide, it traded central bankers for an

un-elected group of miners.

What if you could design a system that would completely alter the economic landscape of the world forever?

The key is how you distribute the money at the moment of creation.

And the first group to recognizethis opportunityand put it into action will change the world.

To understand why you have to look at how money is created and pushed out into the system today.

The Great Pyramid

Today, money starts at the top and flows down to everyone else. Think of it as a pyramid.

In fact, we have a famous pyramid, with a third eye, on the dollar itself.

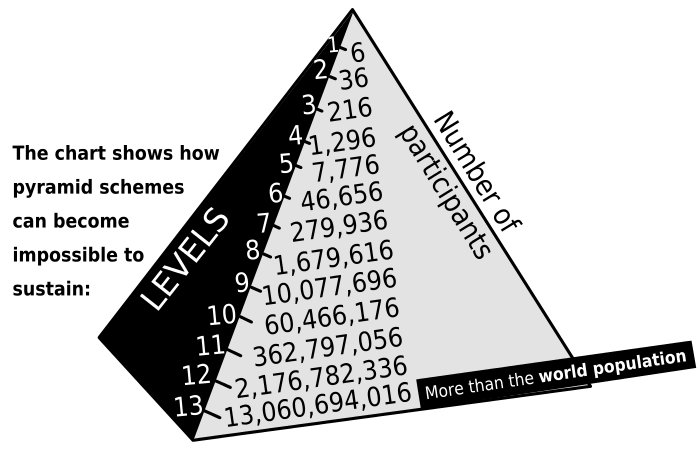

One of the most cliched arguments against Bitcoin is that it’s a Ponzi or “pyramid” scheme.

A pyramid scheme rests on the original creators of the system roping in

as many suckers as possible, paying them for enrolling people in the

system rather than by offering goods and services. Eventually you run

out of people to bring in and the whole things collapses like a house of

cards. A Ponzi scheme is basically the same, in that you dupe the

original investors with fake returns on their initial investment, a la

Bernie Madoff, and then get them to rope in more suckers because they’re

so elated by the huge returns.

The

irony of course is that fiat currency, i.e. government printed money

like the Yen or US dollar, is closer to a pyramid scheme than Bitcoin.

Why? Because fiat money is minted at the top of the pyramid by central

banks and then “trickled down” to everyone else.

The only problem is, it doesn’t trickle down all that well.

It

moves out to a few big banks, who either lend it to people or give it

to people for their labor. In fact, having a job or getting a loan are

the primary methods that people at the bottom of the pyramid get any of

the money. In other words, they trade their current time (with a job) or

their future time (with a loan) for that money. It’s just that their

time is a limited resource and they can only trade so much of it before

it runs out.

Think

of economics as a game. Everyone in the system is a player, looking to

maximize their advantage and the advantage of their team (a company,

their family and friends, etc.) to get more of the money. But to start

the game you need to initially distribute the money or nobody can play. Distributing money sets the playing field.

Now

if you were in charge of the money, how would you distribute it to the

network? You’d want to keep as much of it for yourself as possible, so

you’d set the rules to maximize your own personal advantage. Of course

you would! That’s what anyone in their right mind would do, maximize

their own power to keep it for as long as possible.

That’s precisely what the kings and queens of the ancient world did, and that’s what nation states do today. As Naval Ravikant said in his epic series of tweets on blockchain,

today’s networks are run by “kings, corporations, aristocracies, and

mobs.” “And the Rulers of these networks [are] the most powerful people

in society.”

That’s why every single system in the history of the world has distributed the money in one way:

From the top down.

Because it maximizes the advantage of the kings and mobs at the top.

Unfortunately,

that means most of the money never really leaves the top. It stays

right there, as wasted and frozen potential that’s never realized. There

is little to no incentive for the money to move. Since money is power,

hoarding it is literally hoarding more power and nobody would willingly

give up that power.

In other words, the game is rigged.

What we need is a way to reset the game.

Up until now, our prospects looked very dim.

For example, we could pass a law, like a Universal Basic Income (UBI).

That would give everyone a stream of money, pushing it out across the

entire playing field and giving more people a chance to participate in

the system. If more people can participate, we unlock all kinds of

hidden and untapped value.

How

many great inventors never managed to create their next breakthrough

because they were stuck driving a bus seven days a week to feed their

family, with no hope of free time or any clear path to digging

themselves out of debt? How many great writers went to their graves

never having written their great novel? How many budding scientists

never discovered the cure to cancer or heart disease?

The

problem with all of the plans before now, from UBI to socialism (high

taxes on the rich to spread the wealth across the game) is that to redistribute the money after it’s already been distributed is nearly impossible.

The people with that money rightfully resist its redistribution. And as

Margret Thatcher said “The trouble with Socialism is that eventually

you run out of other people’s money.”

But what if the money is NOT already distributed?

What if we don’t have to take it from anyone at all?

The inevitable outcome of all fractional reserve lending booms is bust.

That’s

the missed opportunity of all of today’s cryptocurrencies.

Cryptocurrencies are creating new money. And unlike credit markets,

which only pretend to expand the money supply, by lending it out 10x

with fractional reserve lending,

cryptocurrencies are literally printing money. And they aren’t loaning

it to people, they’re giving it to them for their service to the

network.

Miners are drafted randomly

to keep the network running smoothly. You might be walking along,

getting coffee and your phone gets called on to secure the network for a

few minutes. After that it goes right back to sleep. As a reward, you

might win new coins for doing nothing but having the application on your

phone. Simple right?

Because everyone is eventually drafted, everyone gets paid, in essence creating a UBI right now.

And that’s just one way.

If

you think about it you can come up with dozens. Oh and don’t get caught

up with thinking the only way to do this is with an ID. Lots of ways to

randomly draft miners without that too. The key is to free your mind of

the “Satoshi box” and think different.

What we really need is to completely gamify the delivery of money, distributing it far and wide at the moment of creation.

Money is a Game. Embrace it.

Give

it out as rewards for using apps, or as distributed mining fees, or as

shared cuts of the mining fees to organizations that provide value to

the network are just a few more ways to do it right. Those are just the

tip of the iceberg. There are thousands of ways but we just haven’t been

thinking about the problem the right way.

In other words, we missed the real power of Satoshi’s creation: the distribution of money.

The first system that truly gamifies the delivery of money will rocket to exponential growth, upending the current system for good. That will set the initial playing field dynamically

and allow players who never would have gotten into the game to compete.

The more people who can participate, the more efficient and valuable

the network becomes.

Right

now, we’re not adding new participants fast enough to the cryptonets of

tomorrow. The system is still vulnerable to the violence hack. Gamified

money is the answer to exponential growth.

If

the system can grow large enough, fast enough, it will become an

unstoppable juggernaut, and the rest of the economic universe will need

to come over to the new playing field.

Once

the Amazons and Google’s of the world join the playing field, their

self-preservation instinct will kick in and they’ll want to protect and

expand it. And this new network will behave differently. Instead of

rewarding just the people at the top, who’ve been rigging the rules in

their favor since the beginning of time, the game will completely reset

with a new set of rules.

What’s best for the whole network, not just the few players at the top, is best.

Those

that join the network and help it grow will thrive and flourish with

it. It will amplify their own value, making it grow faster than at any

point in history. Every ounce they give to the system will magnify their

own rewards.

By

contrast, economies that stand against the network, attempting to

cripple it with arbitrary rules, will pay a heavy price. The system will

stretch across the globe and only the most essential rules will take

root, because in order to upgrade a distributed system, you need vast

consensus across the network. Since people can generally only agree on

big, essential solutions, no self-defeating, narrow-minded rules will be

allowed.

Let’s

say that a country decides to restrict ICOs to their citizens

altogether or make cryptocurrencies illegal. Instead of killing the

network, the rules will blow back on their creators. Only their own

people will suffer, as they won’t be able to participate in the

explosion of new potential that ICOs bring to the table, draining money

out of the economy into rival economies. Even worse, if they make

cryptos illegal, they’ll simply drive that money underground, which will

keep them from getting tax from their citizens, which will starve them

of revenue.

As

the system spreads it will put people back in control of their own

financial power. No one will be able to take your money from you. And

that is a good thing.

Of

course, not everyone thinks so. Some folks always worry that people

will do bad things with this power, like commit crimes. But people will

always do bad things. They do those things now and they always have.

Crippling the system for everyone just to get those people is the height

of insanity. It has never worked and it never will.

Still, some people will never believe that.

They

trust their central powers unquestioningly. All you have to do is wrap

up your argument in “protecting the children” or “fighting terrorism”

and you can generally fool half of the people half of the time about any

terrible policy you want.

Yet

I’ve found that people who see central systems as the answer to

everything have usually lived in a stable central system for their whole

lives.

A few days in an unstable system would change their minds very quickly.

Don’t believe me?

Imagine you lived in Syria right now.

Your

central infrastructure is destroyed, as is your money. You don’t want

the war, but there’s nothing you can do about it. Now your house is

gone, your friends and family are dead, your banks are bombed out and

you’re cast out, adrift, homeless and penniless. Even worse, nobody

wants you. The world has shifted from open borders to building walls

everywhere. You’re not welcome anywhere, you can’t stay where you are and you’re broke.

But what if your money was still there, recorded on the blockchain, waiting for you to download and restore a deterministic wallet and give it the right passphrase to restore it?

How much easier would it be to start your life over?

Cryptocurrencies

finally offer a way for us to control our own destiny. For the very

first time in the history of the world, we have a way to generate and

distribute money without a central power. People will have control over

the money they rightfully earned.

And

even better, instead of setting the playing field so the game is always

rigged, we can set the game up the way it was always meant to be

played, with open competition and flexible rules in a dynamic system

that allows everyone to compete.

But

we need to think big. We need to find a way to distribute the money far

and wide without taking it from everyone else. Do that and we change

the game forever.

That’s what my team is working on. Want to talk? Find us in DecStack.com.