The ECB's LTRO - A Giant Inflationary Push

2 comments | December 21, 2011 | includes: FXE

Banks Borrow Nearly €500 billion

Yesterday there were speculations all day long as to how big the new long term refinancing operation (LTRO) of the ECB would become. As the day wore on, the estimates tended to grow ever larger. We thought that the upper and of the seemingly more daring estimates would likely be hit and that is exactly what has happened. Regarding our thought process in connection with the ECB's policy, we have told our readers from the very day the new easing measures were announced that they should not be underestimated. We have frequently returned to the subject in recent days as the situation has evolved, noting that there was apparently an even bigger inflationary push in the works than hitherto thought. Note here that today's LTRO is only the first of two such operations and that in addition, banks will be able to pledge various other normally difficult to market credit claims with their national central banks in the euro system. As one friend of ours remarked in conversations in recent days (paraphrasing), "this will significantly support the banks and sovereigns in those countries where the primary vector of contagion is from the banks to the sovereign" - such as is for instance the case in Spain. Readers may recall that we have since last year always stressed that in Spain, the banking system and the cost of cleaning it up in the middle of a depression presents an enormous problem for the government.

Regarding today's LTRO, let U.S. first look at a summary from Bloomberg:

“The Frankfurt-based ECB awarded 489 billion euros ($645 billion) in 1,134-day loans, the most ever in a single operation and more than economists’ median estimate of 293 billion euros in a Bloomberg News survey. The ECB said 523 banks asked for the funds, which will be lent at the average of its benchmark rate – currently 1 percent – over the period of the loans. They start tomorrow.“It was obviously an offer the banks could not refuse,” said Laurent Fransolet, head of fixed income strategy at Barclays Capital in London. “It shows the ECB is not out of ammunition and it gives banks security on liquidity for a few years. On the other hand it means banks will rely on the ECB for longer.”

(emphasis added)

Why anyone thought the banks would refuse a big pile of free money is beyond us. After all, Mario Draghi specifically said that "no stigma" would be attached to such borrowing. ThIs code for: "If you borrow from this facility, it will not invite regulatory scrutiny of your institution."

It shouldn't be too difficult to invest money one gets at 1% at a profit, even in today's more risky world in which so-called "risk-free" interest rates have plunged. In addition, as we have pointed out previously, it is an undeniable fact that the fates of banks and governments are in any case tied together for better or worse – and they are lately becoming even more so. Yesterday we were once again discussing with a number of friends how probable it was that the 'Sarko-Corzine trade" as it has been named would be financed with the LTRO's.

At issue is the question whether the banks will be willing to reinvest some of the proceeds from the LTRO's in the "sovereign debt carry trade" in the euro area, thereby simultaneously making a large spread profit, while also helping sovereign bond yields to come down, which in turn will lead to less stringent capital demands on the part of the EBA. This latter point, along with Sarkozy's remarks, is among the dots we are trying to connect. In the meantime (as you will see further below), even more evidence has appeared that points in this direction, although a number of significant counter-arguments remain as well. In short, the question is, will the Ponzi game resume and perhaps even grow. Here is a brief summary of our thinking on the matter:

“One should not underestimate the willingness of banks to play the Ponzi with free money. A fractionally reserved system is after all at all times on the very edge of insolvency. The euro area's especially so – of € 3.92 trillion in sight deposits, only € 211 billion were actually covered with standard money before the most recent halving of reserve requirements. In theory, if more than 4.6% of depositors were to exercise their legal claims to standard money, the banking system would become instantly unable to pay. We say "in theory" because it is of course backstopped by the central bank - as we can in fact once again see in the recent balance sheet explosion.Anyway, why would a system that is constituted like that refuse to gamble with free money? It is the very essence of its business.”

In the Western European legal tradition, this was not always the case. In antiquity a sharp legal distinction between deposit banking and loan banking was made, which is precisely as it should be. As an interesting aside, it was canonical law against usury during medieval times that actually helped to pave the legal way for fractional reserves via the "depositum confessatum" , as J.H. De Soto highlights in his excellent book "Money, Bank Credit and Economic Cycles" [we refer readers to our series on fractional reserve banking for details – Part 1, Part 2 and Part 3].

In brief , the depositum confessatum was a mutuum contract, thIs to say a savings deposit with a fixed term and hence eligible to earn interest. However, since interest payments were circumscribed by usury laws, banks resorted to a trick: the savings deposits were "masquerading" as sight deposits (essentially the exact opposite of what happens today with sweeps) that officially paid no interest. Instead, the banks would pay a fine when the deposit matured, by pretending that they could not immediately pay it on demand. This was in accordance with the laws handed down by the preeminent legal scholars of antiquity, which stipulated that if a banker was found not to have a customer deposit 100% reserved by dint of his inability to pay on demand, he had to pay a fine to his client in addition to the money claim.

You can see where thIs going: once the depositum confessatum became a widespread method of circumventing usury laws, later jurists were easily convinced that a sight deposit in fact represented a "loan to the bank" and not a bailment contract, i.e. a contract for warehousing and safe-keeping. This view serves to this day as the legal basis for fractional reserve banking. As a matter of fact, it was an ex-post legalization of what had previously been regarded as a fraudulent practice.

Not surprisingly, the middle ages were host to a number of banking crises that regularly wiped out large percentages of the banking system in deflationary collapses when these Ponzi schemes blew up (this was obviously prior to central banking and the ability to create literally unlimited amounts of money from thin air).

When the Medici Bank went under in the late 15th century, it held reserves equal to 5% of its deposits. This was an absolutely stunning extreme even for that particular boom-bust sequence, but still better than the reserves of the euro area banking system as a whole today!

Today the banking system has become a moloch that has flagrantly over-traded its capital, is constantly on the verge of collapse and requires ever accelerating inflation to keep its head above water.

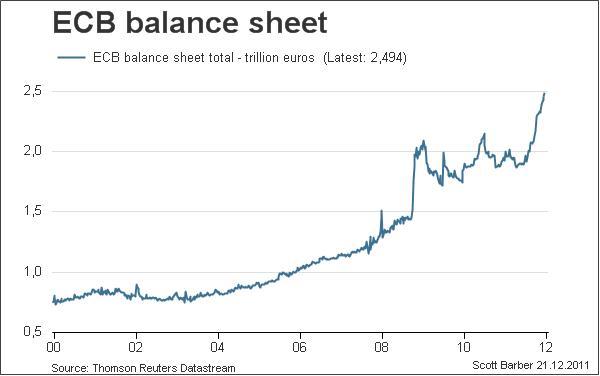

The chart below shows a somewhat longer term view of the ECB's balance sheet (the two crises can be clearly identified) – still pre-LTRO as it were. We will provide the post LTRO chart as soon as is practicable:

(Click to enlarge)

Via Scott Barber from Reuters, a chart of the evolution of the ECB's balance sheet since the year 2000. The two liquidity/solvency crises are clearly discernible. This chart was made yesterday, so the effects of today's LTRO are not yet visible .

Is The Ponzi Game Now On?

Still, in spite of everything we have pointed out above and in previous missives on the subject, one can of course not be absolutely certain that the euro area banks will now use these fresh funds to engage in "QE though the backdoor". Several noteworthy arguments have been forwarded in opposition to this view, such as for instance the fact that banks have lately been rewarded by the stock market for cutting their euro area sovereign debt exposure down. Moreover, since they are experiencing a funding squeeze and are forced to raise more capital, they may use the fresh long term funding mainly to avoid having to sell profitable assets, i.e. as a means to slow down the deleveraging process. All these arguments have undoubtedly merit.

Certainly no-one is forcing the banks to buy more sovereign debt, although we suspect that there is a lot of behind-the-scenes suasion going on, in addition to the broad hints that politicians have made in public, as e.g. those by the "pro QE" French president Sarkozy. In politics it is always important to read between the lines and separate the meaningless chatter from the handful of things that actually count – nothing happens by coincidence.

Consider how the Sarkozy-Merkel dispute over the ECB's role in the sovereign debt crisis was resolved: Sarkozy agreed to simply "back down" and no longer mention his demands in public, so as to "preserve the independence of the ECB". What course this independent supra-national government agency then actually embarks on is up to its governing council, but the monetary bureaucrats surely can take a hint as well as anybody. Besides, we feel fairly certain that the issue was discussed with them as well. From the point of view of the ECB, the biggest danger is always that its management of "inflation expectations" may eventually run into problems. Therefore it regards it as extremely important to keep up the impression of independence, since thIs presumed to reassure economic actors in the euro area that the vaunted "price stability" policy is not in danger due to the whims and needs of over-indebted governments.

In short, like every modern central bank, the ECB wants to be free to inflate as much as is possible without people noticing, so the speed and degree to which the purchasing power of the money it issues declines is high up on its list of priorities. Inflation of the money supply can very quickly become quite counterproductive from the point of view of the interventionist if and when the markets react negatively to repeated deployments of the printing press.

Note that the ECB has frequently stressed that it wants to keep bank credit available to "households and companies" in the euro area – it never mentioned that the banks should buy sovereign debt. Alas, it seems fairly certain that both objectives are part of the plan. Consider now that in Qu.1 of 2012, some € 530 billion in bank and sovereign bond will mature and require rolling over. This seemed an extremely daunting prospect hitherto. Following the LTRO, it is far less so.

Further from Bloomberg's summary:

“Barclays estimates the loans will inject 193 billion euros of new money into the system, with 296 billion euros accounted for by maturing loans. The ECB also lent banks $33 billion for 14 days in a regular dollar offering, up from $5.1 billion a week ago, and 29.7 billion euros for 98 days.The euro jumped half a cent to $1.3198 before slumping to $1.3080 at noon in Frankfurt. Spanish two-year notes extended a decline, snapping an eight-day gain and sending yields seven basis points higher to 3.42 percent. Italian notes also declined, pushing the yield nine basis points higher to 5.06 percent.Italian and Spanish government bond yields have dropped since the ECB announced the loans on Dec. 8 as banks buy the securities to use them as collateral. French PresidentNicolas Sarkozy has suggested banks could use the loans to buy even more government debt.“What the ECB wants is that the funds be used by banks to keep handing out loans,” said Michael Schubert, an economist at Commerzbank AG in Frankfurt. “But there’s a second argument, which is to do carry trades by borrowing on the cheap at the ECB and buying sovereign bonds. We don’t know what the banks are using the money for.”

(emphasis added)

Nearly €200 billion in additional liquidity is quite a lot. Consider that the sovereign borrowing requirements frequently cited are the gross, not the net amounts. Most of the borrowing is to roll over maturing debt, so around the time bond auctions occur, there is also an inflow from the repayment of maturing debt. In light of this, the € 200 billion in excess liquidity created by LTRO number one (a second operation is scheduled for February next year) is quite a big deal. In fact it is almost equal to the amount of unsecured bank bonds maturing in the first quarter (an estimated € 230 billion). It also seems unlikely that the banks won't find a single buyer when they issue bonds early next year, especially if the crisis pauses for a while.

As Bloomberg continues in this context:

“ECB Vice President Vitor Constancio in a Dec. 19 interview predicted “significant” demand for the loans as banks face “very high refinancing needs early next year.” Some 230 billion euros of bank bonds mature in the first quarter of 2012 alone, ECB President Mario Draghi told the European Parliament this week.“Banks represent about 80 percent of lending to the euro area,” Draghi said. “The banking channel is crucial to the supply of credit.” He predicted banks will experience “very significant funding constraints” for the “whole” of 2012. Banks from the euro region need to refinance 35 percent more debt next year than they did this year, according to a Bank of Englandstudy. Lenders have more than 600 billion euros of debt maturing in 2012, around three quarters of which is unsecured, the study says.The ECB is focusing on greasing the banking system to fight the debt crisis as it resists calls to increase its bond purchases to reduce governments’ borrowing costs. Today’s lending exceeded the 442 billion euros awarded in the ECB’s inaugural 12-month loan in 2009. The central bank will offer a second three-year loan in February and borrowers have the option of repaying the funds after a year.“It’s very significant and very helpful for the banks,” Jacques Cailloux, chief European economist at Royal Bank of Scotland Group Plc in London, told Bloomberg Television. “But it’s not going to bring about a turning point in this crisis.”

(emphasis added)

We would certainly agree with Mr. Cailloux that this does not represent a true "turning point" in the crisis. It should be clear that the main effect will be to buy a little bit more time. The fundamental problems besetting the euro area can ultimately not be resolved by revving up the printing press. Solvency and liquidity are two quite distinct issues, but as we know, banks are very sophisticated when it comes to "extend and pretend" games.

What it does represent is the chance for a pause in the crisis, i.e., it gives everybody more time to dig an even bigger hole. What is also noteworthy about all thIs that it confirms something we have often stressed: the root of the current crisIs in fact the credit expansion and boom engendered by the fractionally reserved banking system prior to the 2008 caesura. The crisis goes well beyond a mere sovereign debt crisis in that sense – it is more profoundly systemic in nature and concerns the monetary system itself. Concurrently with the liquidation of malinvested capital, the unsound credit supporting these malinvestments needs to be liquidated as well. ThIs precisely the process the ECB's latest measures attempt to arrest or at least delay.

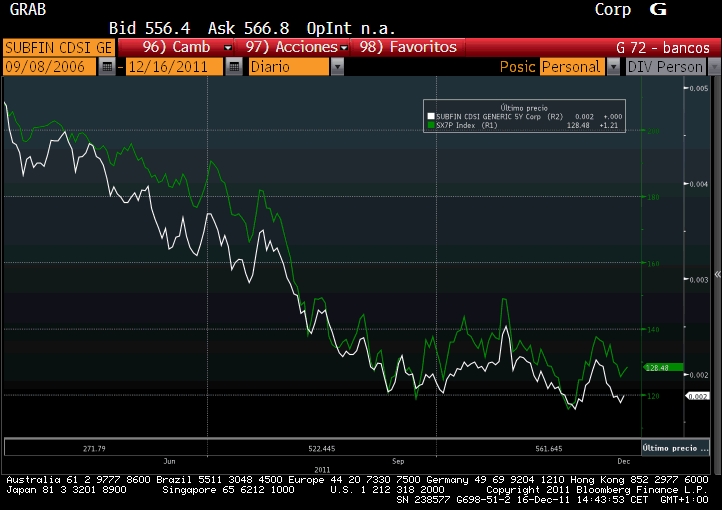

(Click to enlarge)

A chart showing the inverse of the Markit i-Traxx subordinated bank CDS index vs. the euro area bank stocks index. The prices of bank stocks are closely correlated with market perceptions about default risk.

A long term chart of the growth in non-performing loans in the Spanish banking system via a recent research report by BNP – in spite of Spain's banks being past masters at hiding their losses, these NPLs have begun to climb sharply. Most of them are mortgages and loans to real estate developers.

Spain's deposit growth has turned negative as a result of bank credit growth turning negative. Spain's banks get an ever larger percentage of their funding from the ECB these days.

Is is clear from the above that Spain's banks – and this goes of course for the banks in all the other "PIIGS" nations too, even though the details of their problems differ from case to case – should be more concerned with getting their leverage down and generally getting their house in order rather than embarking on yet another carry trade. And yet, from the point of view of the banks, things may look a bit different. As noted before, the fate of banks and their sovereigns is in any event closely intertwined. A bank that may one day require a government bailout will go under anyway if the government debt crisis worsens further. So it has actually nothing to lose by adding to its holdings of bonds issued by said government. They will both sink or swim together no matter what.

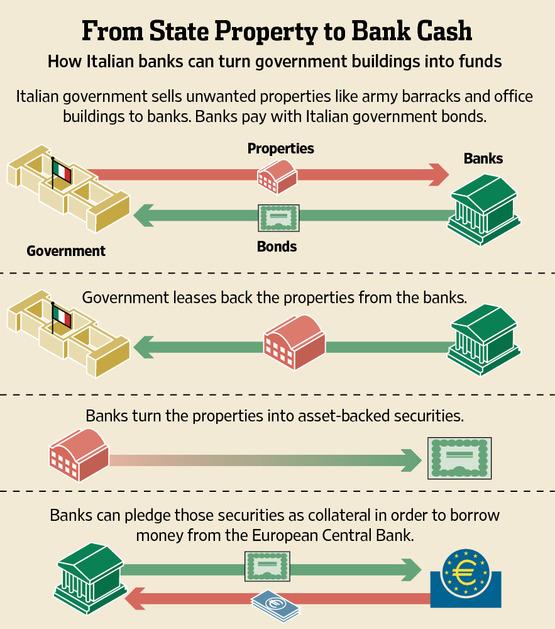

A new story has emerged yesterday that illustrates what actions governments and banks in the euro area are taking behind the scenes to ease the bank funding crisis. It should be clear that one of the unstated objectives of these activities is to free up money for the purpose of banks adding to their sovereign debt holdings. While these are all piecemeal actions, they certainly tend to cement the interconnectedness between banks and governments even further.

As the WSJ reports:

“Governments in Europe are tying themselves in knots to prop up their banks, desperate to blunt the cost and embarrassment of a fresh wave of taxpayer-funded bailouts.In Italy, for example, the government is encouraging banks to buy public properties that the banks then can use to borrow money. As part of a broader deficit-reduction program in Portugal, the government essentially is borrowing money from bank pension funds and could use some of the funds to help state-owned companies repay bank loans. Governments in Germany and Spain also are using unorthodox measures to support their ailing banks.The unusual moves come as euro-zone countries are under growing pressure to reel in soaring borrowing costs by showing investors in government bonds that their budgets are under control. In addition, bank bailouts are politically toxic, especially for governments that have sought to reassure markets about the health of their banking systems. Some economists say such moves aren't an adequate substitute for a broader rescue package that would include recapitalizing the lenders and helping them issue new debt.”[….]A provision tucked into the Italian government's budget law last month is designed to defuse some of those pressures. It allows the banks to use their government bonds to purchase army barracks, office buildings and other state-owned real estate that the government has been trying to sell. The government would then lease the properties back from their new owners. And the banks can package the income-producing properties into asset-backed securities, which can be pledged as collateral with the ECB in exchange for loans, analysts say.Italy's real-estate-for-sovereign-bonds maneuver also gives a boost to the government. Not only can it rid itself of unwanted properties, but the government also will be able to retire the bonds that banks use to purchase the real estate—thereby reducing Italy's heavy debt load.”

(emphasis added)

The article brings several more examples illustrating the maneuvers in other countries as well (such as e.g. the "redirection" of pension funds by Portugal's government), but the point remains that we can see here that the various euro area governments and their banks are closely cooperating in an attempt to defuse the pressures on both the bank funding issue and the sovereign debt crisis. The banks are probably being told by their governments "if you want our help, you better show up when there's a bond auction".

(Click to enlarge)

Backdoor bank bailout, Italian style: how to offload government buildings on the ECB's balance sheet and thereby ease both bank funding pressures and create a more favorable supply-demand situation for the government's debt.

As Reuters reported yesterday, Italian banks are also using state guarantees for their own bonds to make them presentable as ECB collateral.

“More than 10 Italian banks, including major lenders, are looking to apply for the European Central Bank's new ultra-cheap three-year loans by using state-guaranteed bonds as collateral, a source close the situation told Reuters on Tuesday.A second source confirmed all the main Italian banks had requested state guarantees for bank bonds under a new scheme -launched by Italy's emergency government – aimed at lowering funding costs for lenders.-"There has been interest in state-guaranteed bonds. There have been requests by more than 10 banks that were approved. Banks are doing this … to present it as collateral for the ECB loans," one of the sources said.”[….]The ECB hopes its first ever limit-free, ultra-cheap and longer funding will help bolster trust in banks, ease the threat of a credit crunch and tempt banks to buy Italian and Spanish debt.”

(emphasis added)

Now, the ECB never said that it wants to "tempt banks to buy Italian and Spanish debt", but who can doubt in view of all these machinations that "QE through the backdoor" is in fact a major goal?

The Counter-arguments

The big question is though whether it will actually work. There was an extensive discussion of the counter-arguments at the FT's Alphaville blog, which highlights all the perceived problems with the "carry trade" idea. See: "The carry trade and the goldilocks LTRO".

A few pertinent quotes:

“The FT has already reported (pdf) on how hesitant banks are about buying ever more sovereign debt. In fact they outright dumped €65bn of bonds in just nine months. Hopes that banks would hold the hand of the sovereigns that back them continue to dim, as the Sarko carry-trade looks increasingly less likely in advance of this Wednesday’s offer of cheap 3-year ECB financing.”The presumption that banks are going to use the 3-year Long Term Refinancing Operation (LTRO) to buy sovereign bonds comes not just from the dreams of certain politicians, but also from the observation that yields at the short end of peripheral curves have come in dramatically.Is this the result of banks buying up the high yielding bonds that they will soon be able to fund exceptionally cheaply?[...]Not so much, say the analysts at SocGen in their Rates Strategy daily this Monday. There are many factors at play, and true, one of them may be the anticipation of banks putting on carry trades, but the expectations may not transform into reality.For one thing, banks are going to have to find a way to fund their existing asset holdings — to the extent that they don’t deleverage themselves into nothingness, that is — and a good portion of the current funding for them will roll off in 2012. SocGen points out that for eurozone banks in 2012, €250bn of senior unsecured bank bonds will mature, along with €83bn of government guaranteed debt, plus €19bn of subordinated debt.Seeing as the unsecured market is somewhere between frozen and inaccessibly expensive, the most relevant candidate for the replacement of that debt is reckoned to be around €185bn of covered bond issuance, a figure which the analysts acknowledge may well be a bit on the high side (though at least it will be supported by another ECB programme to specifically prop up that market).The rest of the funding needs to come from somewhere. And, well, the ECB is offering …”

(emphasis added)

We think that this perhaps underestimates the degree to which governments can and will exert pressure on the banks. When all the euro area governments are extending a helping hand to the banks, one must assume this doesn't come for free.

Nevertheless, the fact remains that the commercial banks cannot beforced to buy more sovereign debt and that the trend has lately been for them to offload it. Moreover, sovereign risk remains extremely high, and the probability of a break-up of the euro area remains very high as well. In all likelihood sovereign debt holdings will shift within the euro area banking system, with domestic concentration increasing.

In the final analysis, all these contortions are an attempt to con the markets one more time. The banks face considerable uncertainty when engaging in this carry trade – if the sovereign debt crisis flares up again, their losses will increase. Nevertheless, the mountain of liquidity unleashed by the ECB will definitely have an effect on prices somewherein the economy. Our best guess at this point in time would be that it buys some time and leads to another brief lull in the crisis. It will be very telling in this context how the markets react to the next slew of downgrades of various sovereigns in the euro area.

More Ratings Warnings – The EFSF Comes Under Scrutiny

Fitch has just released a warning on the credit rating of the euro-area's bailout fund, the EFSF. This warning must be put into context: it would make no sense to issue it unless the probability was high that Fitch will eventually dispense a number of sovereign downgrades, with France high up on the list of candidates.

As the WSJ reports:

“The triple-A debt rating of Europe's temporary bailout fund largely depends on France and Germany retaining their triple-A status, ratings agency Fitch warned Tuesday, adding that the agency's revision last week of its outlook on France to negative implies that the fund is at a greater risk of a downgrade."We affirmed France's triple-A status but warned that there is a slightly greater than 50% chance of a downgrade within the next year or two. This is therefore also the case for the triple-A ratings assigned to the [European Financial Stability Facility's] debt issues, unless additional credit enhancement mechanisms are introduced," Fitch said.Fitch's comments follow a warning by Standard & Poor's Corp., which said Dec. 6 that it could strip the EFSF of its triple-A rating by up to two notches, if any of the similarly rated countries that guarantee the fund were also downgraded.The triple-A ratings assigned to EFSF debt issues rely on the €726 billion ($944 billion) of irrevocable and unconditional guarantees provided by the euro-zone states, and on the conservative guidelines the EFSF sets itself regarding debt management and liquidity risk, Fitch said.France and Germany provide €369.6 billion — or more than 80% — of the guarantees and over-guarantees to the bailout fund. While such warnings from ratings firms have to some extent been expected, they have created much uncertainty, with market participants awaiting further clarification.[…]France is the most exposed of the triple-A countries in the euro zone to the currency bloc's deepening sovereign-debt crisis. It provides €158.5 billion of guarantees as well as over-guarantees to the EFSF guarantee pool under the framework agreement, Fitch said.”

(emphasis added)

It is of course no big surprise that the EFSF finally comes under more scrutiny by the rating agencies. We believe that the ratings of France and the EFSF harbor great potential to become the next "crisis trigger".

One would normally assume that the markets have already discounted a coming downgrade of France's government debt and to some extent thIs true: both CDS spreads and OAT yields indicate a certain degree of discounting has indeed taken place. However, recent experience indicates that this discounting is rarely complete. Usually we see both the credit markets and so-called "risk asset" markets take an additional pounding when a significant new downgrade is issued, even if it was widely "expected". This should be especially true in this particular case, where the EFSF would become subject of an automatic downgrade in the wake of a downgrade of France. For the moment, Fitch at least has given France more time, but it is not yet certain whether Standard & Poors will be similarly generous.

In summary, we would expect the ECB's LTRO's to create a lull in the crisis, but it won't help to actually overcome it. The highly likely lowering of the credit rating of France and by implication of the EFSF, are high up on our list of the next potential crisis triggers, but we will of course have to wait and see how the markets actually react when the time comes.

Addendum:

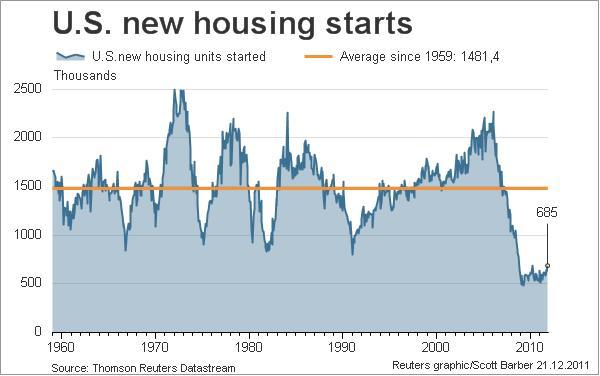

Below is a long term chart of U.S. housing starts published by Reuters yesterday. This shows how little the recent improvement in housing starts amounts to in the longer term context. Still, it does appear as though housing starts are trying to put in at least a short to medium term bottom. Overall the performance is still so bad though that the recent improvement will probably not suffice to dissuade the new, even more "dovish" incarnation of the FOMC from embarking on another round of MBS monetization next year.

(Click to enlarge)

U.S. housing starts: the recent improvement in the longer term context.

Charts by: Bloomberg, Reuters, BNP, WSJsa

Nessun commento:

Posta un commento